Zambia: Upgrade to category 6/7 for MLT political risk

Highlights

- After a profound financial crisis and severe drought, economic prospects are favourable again.

- Zambia’s resilience stems from substantial current account revenues, strong policy performance, long anticipated progress in debt restructuring and restoring investor interest.

- Major risks include climate shocks, adverse changes in copper price, and loss of fiscal discipline or reform momentum in the run-up to the 2026 elections.

- Credendo has upgraded Zambia’s medium- to long-term political risk classification from category 7/7 to 6/7.

Pros

Cons

Head of State

Description of electoral system

Population

GDP per capita

Income group

Main export products

Dealing with the aftermath of the 2020 default and a devastating drought

Former president Lungu came to power in 2015, after which corruption, oppression and economic mismanagement spiralled. Double-digits inflation raised the cost-of-living, and unsustainable borrowing plans – marked by a lack of transparency – combined with a drop in commodity prices pushed the country towards a public debt crisis. In November 2020, Zambia defaulted on its external public debt (Eurobond default) leading to a profound financial and economic crisis.

In August 2021, President Hichilema was elected and delivered on stabilising the political scene after years of mismanagement. His government’s ability to negotiate a restructuring deal which moved the country out of a lingering debt crisis has earned him general public approval. The current administration is committed to fiscal consolidation, positive engagement with the private sector and policy reforms under the IMF Extended Credit Facility programme (August 2022 – October 2025), enabling a recovery in investor confidence.

Since January 2024, Zambia has been dealing with the worst drought the Southern African region has faced in over a century. It is driven by El Niño and intensified by climate change, through the disruption of the 2023 – 2024 rainy seasons. The ongoing drought is affecting agricultural production, hydroelectric power generation and raising water and food insecurity risks for millions of people while emergency aid remains underfunded due to cuts in international solidarity spending. There is cautious optimism regarding the 2025 rainy season, which has been influenced by a weak La Niña resulting in wetter conditions for the region, yet water levels remain critically low in many parts of the country and power outages continue. The drought will shape critical conditions for President Hichilema’s re-election bid in the August 2026 general elections, as socio-economic circumstances have been gravely affected across the country. Nevertheless, according to the IMF, social protection spending has helped cushion the impact of the drought and price-hikes on more vulnerable households.

Zambia is no longer considered as being ‘in debt distress’

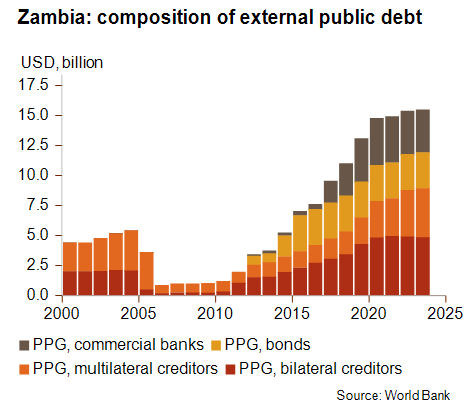

The public debt restructuring process under the G20 Common Framework for Debt Treatment started in 2021 but has been criticised for its slowness, which is due to disputes among creditor countries on the one hand and the magnitude of commercially held government debt on the other. In June 2023, Zambia reached a MOU agreement with its official bilateral creditors committee under the G20 Common Framework to restructure roughly USD 6.3 billion. One year later, Zambia also successfully completed the exchange of its outstanding Eurobonds, another significant positive step in recovering its debt sustainability. Moreover, in early 2025, an ‘in principle’ agreement was reached with some of the external commercial creditors. Under its baseline scenario, the IMF assumes that residual claims of other external commercial creditors (including Chinese banks) will be processed in line with the restructuring strategy under the IMF programme and thus revised the overall risk of debt distress from ‘in debt distress’ to ‘high risk of debt distress’ (yet sustainable) in December 2024. Although Zambia is still in a ‘post-default recovery stage’, it is no longer in debt distress and prospects are improving significantly.

Zambia’s public finance figures reflect that there has been a turnaround thanks to the restructuring process, fiscal reforms, spending compression and optimistic prospects for copper production, which can partly offset the grave impact of the ongoing drought. Due to the high reliance on foreign currency denominated public debt, periods of kwacha depreciation pushed the government debt stock beyond 150% of GDP in 2020. As Zambia has been locked out of international capital markets since 2020, the government became more reliant on domestic debt, which accounts for almost 40% of the total stock today. The overall fiscal deficit has dropped since 2022 and the public debt stock should fall below 100% of GDP again this year.

Strong export projections support liquidity recovery

Zambia is Africa’s second largest copper producer, and copper accounts for approximately 60% of current account revenues. In 2024, Zambia’s copper production increased by 12% despite operational challenges linked to drought-induced energy shortages, and production will be further boosted in the near term thanks to increased interest from foreign investors. Indeed, copper is an essential and strategic mineral in the global renewable energy transition (EVs, wind turbines, solar panels, etc.) as well as other advanced technologies. Zambia’s main export destinations are Switzerland (27% of goods exports, mainly copper), China (14% of goods exports, mainly copper), UAE and India. As less than 1% of goods exports are directed to the US, the direct impact of trade tariffs is expected to be limited. Zambia is nevertheless hit by the cuts in USAID due to its longstanding reliance across key sectors (education, health and agriculture). In fact, in 2023 about 70% of all bilateral aid (2.3% of GDP) came from the US.

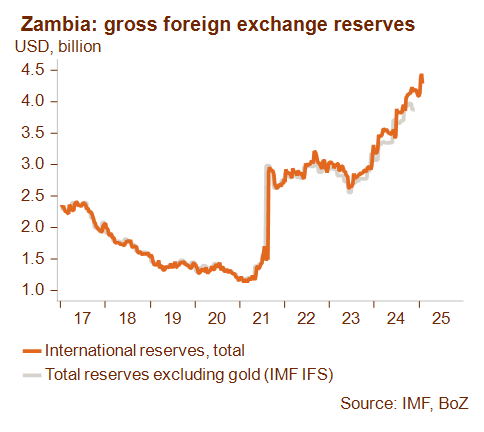

Since 2016, the accumulation of large financing gaps on the external balance – caused by trade imbalances and capital flight – together with stacking debt servicing pressure, led to a continued fall in foreign exchange reserves, down to a record low of USD 1.2 billion following the Eurobond default at the end of 2020. Thanks to the allocation of significant IMF financial support, the stabilisation of the political scene and recovering copper revenues, foreign exchange reserves have seen a strong and continued recovery, surpassing USD 4 billion or four months of imports in May 2025. Although the value of the flexible kwacha was still under substantial pressure in 2023, losing 42% against the US dollar, it only lost 7% in 2024 and actually gained 13% against the US dollar during the first half of 2025. The liquidity and currency recovery have been made possible through fiscal discipline, progress in the debt restructuring process and a tight and credible monetary policy stance.

After displaying small deficits in 2023 and 2024, the current account is projected to move towards equilibrium this year and a widening surplus in the medium term driven by substantial critical minerals exports. Despite significant capital outflows, increasing foreign direct investments should support the external balance of payments. The total external debt stock peaked in 2020 and is set to tumble in coming years to an estimated 75% of GDP by 2026. Also, the external debt servicing burden should drop to a sustainable 12% of current account revenues this year, thanks to reduced debt servicing obligations following the restructuring agreement.

Despite great global uncertainty, Zambia’s growth performance is strong

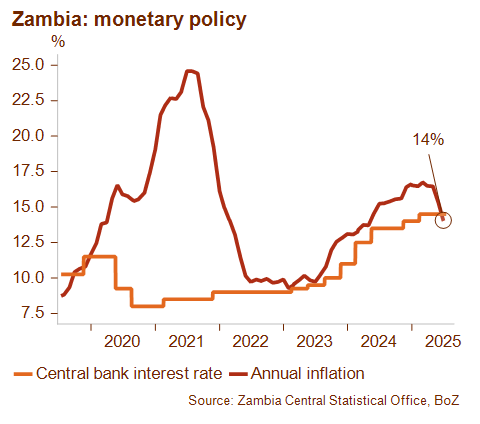

Despite the detrimental drought that ravaged the country, Zambia’s economy showed resilience and grew by 4% in 2024 as the contraction in agriculture was less severe than initially expected. Economic growth should reach 6% and more in 2025 and 2026 driven by mining activity, infrastructure investments, gradual electricity generation recovery and growing private sector participation. Inflation has been high for years, driven by food inflation, supply shortfalls and kwacha depreciation but is expected to come down to 11% by the end of 2025 (year-on-year). Should the Bank of Zambia maintain its tight monetary policy going forward (policy rate at 14.5%), inflation could be tempered to around 7% in the coming years.

Zambia’s outlook is favourable thanks to positive current account projections, strong policy performance and the agreement on debt restructuring. However, there are still some major risks to the outlook, such as slow recovery of rainfall levels, more adverse climate shocks, volatility of global copper prices and challenged fiscal reform implementation in the run-up to the 2026 general election.

Analyst: Louise Van Cauwenbergh – l.vancauwenbergh@credendo.com