Sub‑Saharan Africa: An evolving debt landscape brings new challenges

Highlights

- After substantial debt relief in the mid‑2000s, public debt levels in Sub‑Saharan Africa have risen again to historically high levels.

- Debt‑service burdens continue to rise, increasingly crowding out fiscal space for investment, climate adaptation and social spending.

- Fragmented creditor bases and non‑traditional lenders have made debt relief negotiations longer, more complex and more uncertain.

- Levels of external debt are an important factor in Credendo’s medium- to long-term political risk classification.

Historical debt dynamics and their consequences

While short‑term disruptions often command attention, more gradual shifts in Sub-Saharan Africa’s debt profile have been quietly reshaping underlying vulnerabilities over the last decades.

After independence in the 1960s and 1970s, many Sub‑Saharan African countries accumulated debt to finance development and state formation. This debt build‑up accelerated after external shocks in the late 1970s and became acute in the early 1980s, when higher global interest rates raised debt‑servicing costs just as lower commodity prices led to lower revenues for commodity‑exporting economies.

By the mid‑1990s, debt burdens had become unsustainable. In several countries, debt service absorbed over 30% of public revenues, severely limiting fiscal space and constraining spending on essential services and investment.

A series of debt relief initiatives followed. The launch of the Heavily Indebted Poor Countries (HIPC) Initiative in 1996 and the Multilateral Debt Relief Initiative (MDRI) in 2005 led to large‑scale debt cancellation for many Sub‑Saharan African countries, substantially lowering debt stocks and debt‑service burdens and effectively providing a partial fiscal reset.

Today, debt levels in Sub-Saharan Africa are once again high by historical standards, bringing debt vulnerabilities back into focus. Beyond the rise in debt itself, the composition of borrowing has changed over the past two decades in a number of different ways. Private creditors and new bilateral lenders have taken on more prominent roles, while multilateral lenders continue to play a major role and domestic public debt has increased. This article will further examine the debt trends in Sub-Saharan Africa.

Rise of domestic debt

One notable trend is the growing importance of domestic debt in total public debt. Traditionally, many countries in Sub-Saharan Africa relied heavily on external loans (often denominated in foreign currency) from bilateral and multilateral creditors. However, over the past decade, many countries have pivoted towards domestic borrowing, issuing more debt in local currency to domestic banks, pension funds and local financial markets.

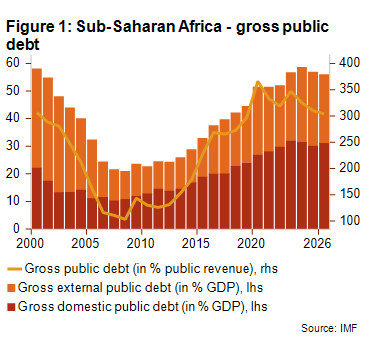

Domestic public debt now accounts for over half of total public debt in Sub‑Saharan Africa (see Figure 1) and has become the driver of rising debt service costs in several countries. In the wake of the 2022 tightening of global financial conditions, several countries that lost access to international markets relied on domestic bond issuance to meet their financing needs.

Increasing local‑currency borrowing does offer certain advantages. By shifting financing into domestic currency, governments can reduce exchange‑rate risk and limit the need to draw on scarce foreign‑exchange reserves for debt service. Domestic borrowing can also provide a degree of insulation from swings in foreign investor sentiment, a point illustrated by the fact that no Sub-Saharan sovereign was able to issue Eurobonds between April 2022 and January 20241, amid rising US interest rates.

However, this shift also introduces new vulnerabilities. Domestic interest rates are generally high, with the median African government paying around 8.8% on new domestic debt in 2024, even if elevated inflation can partly mitigate this interest burden in real terms for some countries. Moreover, domestic debt generally carries shorter maturities than external loans, increasing rollover risk since governments must refinance maturing obligations more frequently, potentially at higher rates. Ghana is a clear illustration of this: following its domestic debt restructuring in 2023, the government had to rely largely on short‑term treasury bills amid subdued investor confidence.

Perhaps the most worrying consequence of this evolution is the growing sovereign-bank nexus. Large holdings of government securities by domestic banks in countries such as Angola, Kenya, Nigeria and Zambia have tied the health of the financial sector to government creditworthiness, while potentially crowding out private sector lending.

Multilateral and bilateral debt

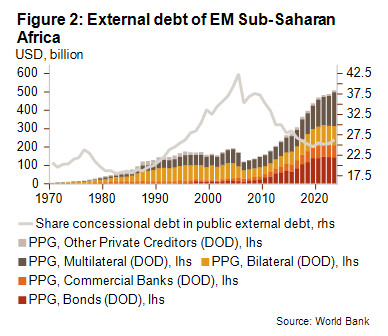

Official lenders – multilateral institutions and bilateral government creditors – remain crucial in Africa’s public external debt composition, but their roles have shifted over time. Multilateral institutions such as the IMF, World Bank, African Development Bank and others have significantly increased lending to Sub‑Saharan Africa, especially during crises. Multilateral debt has therefore been one of the fastest‑growing components of external public debt over the past decade. For Sub-Saharan Africa’s emerging market (EM) economies, it rose from about USD 79 billion in 2014 to USD 198 billion in 2024 – roughly a 150% increase, as illustrated in Figure 2. Multilaterals are now the single largest creditor group in emerging‑market Sub‑Saharan Africa. These loans tend to be on concessional terms (low interest rates and long maturities), but the sheer volume means that repayment obligations are mounting; according to the World Bank, multilateral debt amortisations for Africa climbed from USD 4.0 billion in 2018 to USD 12.2 billion in 2024, and are projected to reach USD 16.9 billion by 2028. This front‑loading of crisis lending has raised concerns about a debt‑service hump coming due in the second half of the 2020s.

In contrast, bilateral external public debt (loans from individual countries) has become less prominent. Traditional Paris Club creditors (such as France, UK, US and Japan) reduced lending after extensive Paris Club debt cancellations in the 2000s. At the same time, a new group of bilateral lenders emerged outside the traditional Western creditors, chief among them China, alongside countries such as India, Türkiye and several Gulf states.

China, in particular, rapidly expanded its engagement with Africa from the early 2000s under its “Going Out” strategy and later the Belt and Road Initiative, evolving from a marginal player into, by some measures, Africa’s single-largest bilateral creditor. Chinese financing helped to fill major infrastructure funding gaps, but it also altered debt dynamics, as many loans were extended on less concessional terms and, in some cases, backed by collateral or commodity‑linked repayment structures.

Chinese loan commitments peaked around 2016 and have declined markedly ever since. Reflecting both the slowdown in Chinese financing and the retreat of traditional Paris Club lenders, bilateral official debt peaked at around USD 109 billion in 2021, before falling to approximately USD 104.5 billion by year-end 2024.

The growing importance of private creditors

Another important shift has been the growing role of private creditors in African public debt. Following large scale debt relief and against the backdrop of low global interest rates and abundant liquidity, many African governments accessed international capital markets for the first time. By 2021, at least 21 Sub Saharan African countries had issued Eurobonds, compared with virtually none prior to 2006. As a result, a rising share of EM Sub-Saharan Africa’s external public debt was owed to commercial lenders and investors.

Figure 2, discussed above in relation to multilateral creditors, also highlights the growing role of private creditors in external debt, both through sovereign bond issuance and lending by commercial banks.

Consequences of the changing landscape

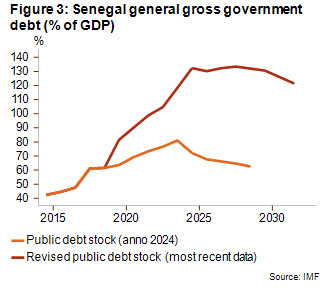

The involvement of multiple private and non-traditional lenders, combined with the increasing complexity of debt instruments, has significantly complicated the process of monitoring public debt. Some governments accumulated “hidden debts” – loans not reported transparently. A notorious example occurred in Mozambique, where state-owned companies secretly took on USD 2 billion in commercial loans (with government guarantees) for dubious projects, leading to a scandal and default in 2016. More recently, Senegal’s debt rose drastically after previously unreported obligations (infrastructure loans by state enterprises) came to light (see Figure 3).

The evolving landscape has also complicated debt resolution processes. In earlier crises, resolving unsustainable debts often meant convening a relatively small group of official bilateral creditors (e.g. the Paris Club) to negotiate debt treatment. Today, governments in distress must negotiate with a fragmented array of creditors, including private bondholders, commercial banks and non-traditional bilateral lenders such as China, India and Gulf countries. This has made debt treatments more protracted, complex and uncertain.

Zambia’s 2020 default illustrates the challenges of this new debt environment. The country spent over three years negotiating a restructuring involving a diverse set of creditors, including Eurobond holders, Chinese lenders and multilateral institutions. Ghana’s 2022 default followed a similarly complex path: while a comprehensive domestic public debt exchange was implemented early on and an agreement with the official creditors committee was found in early 2024, negotiations with external private creditors have dragged on. Ethiopia underscores the same coordination challenges: despite entering the G20 Common Framework for Debt Treatments in early 2021, its restructuring is still unresolved, complicated by geopolitical tensions and persistent disagreements among creditors.

Outlook

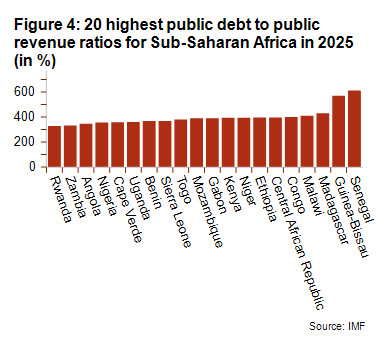

Sub-Saharan Africa’s public debt evolution has come full circle in many respects. After the extensive debt relief of the mid-2000s, debt burdens crept up and are now once again high in relation to governments’ revenue in many countries (as can be seen in Figure 4). Several nations are at a high risk of debt distress according to the IMF Debt Sustainability Analysis.

Public debt ratios in the region have stabilised at around 58% of GDP, as can be seen in Figure 1, although the regional average can mask large differences. For example, Cabo Verde and Mozambique have public debt loads exceeding 100% of GDP, while a country such as DR Congo (close to 20%) maintains a very low debt burden relative to GDP. Crucially, debt service costs are still rising. By 2025, the external debt service-to-revenue ratio will average roughly 18% (up from 15% in 2024), and several countries (Guinea-Bissau, Malawi, Sierra Leone) face especially severe public debt-service burdens exceeding 35% of revenues.

Limited fiscal space crowds out vital spending, constrains policy responses to unforeseen shocks, and increases macroeconomic fragility and default risk. This loss of fiscal space is particularly concerning in an environment of rising global interest rates and given the scale of investment needs, including infrastructure, social spending and climate adaptation, at a time when many Sub‑Saharan African countries are highly exposed to climate‑related shocks.

Elevated debt‑service burdens can also carry political implications, as efforts to restore public debt sustainability often require tax increases or expenditure restraint. The protests in Kenya against the 2024 finance bill illustrate the tensions between the need for fiscal consolidation and popular resistance to higher taxes or spending cuts, highlighting how debt pressures can spill over into social and political instability.

Analyst: Jonathan Schotte – j.schotte@credendo.com

1 Gabon did conduct a USD 500 million “debt-for-nature” swap in 2023, and while it was an external sovereign bond issuance in foreign currency, it was an unconventional one.