Global supply chains in chaos after one month of conflict in the Middle East

The Middle East conflict and effective closure of the Strait of Hormuz have emphasised the global economy’s dependence on exports from Gulf Cooperation Council (GCC) countries– not only in oil and gas, but also in other products – which are crucial to various supply chains. Disruptions in these exports have already caused damage to supply chains in terms of shortages, delays in production and increase in production costs across the energy, manufacturing and transport sectors.

Disruptions are becoming more apparent as the last maritime shipments from GCC countries have arrived and stocks are dwindling. Even if the conflict ends soon, supply chains could take months or even years to recover, particularly if infrastructure has been damaged. Time will be required to repair the infrastructure, to clean and restart equipment that has been put on hold as a precautionary measure, and to clear bottlenecks in ports. At this point, the risk of escalation remains high, which would only prolong the closure of the Strait of Hormuz and cause further damage to energy and other infrastructure.

- Crude oil and gas

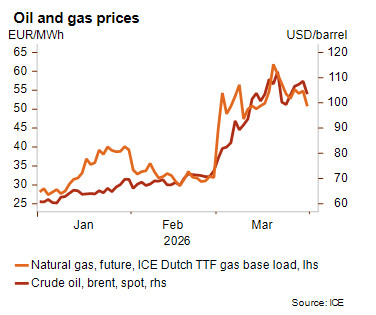

Given the closure of the Strait of Hormuz, through which about 20 to 30% of global oil and 20% of LNG pass, and damages to energy infrastructure, energy prices have surged. The Brent crude oil price has risen by about 50% since 28 February, when the attacks started, and the TTF spot price (benchmark for the gas price in Europe) has risen by about 60%.

The ongoing conflict in the Middle East has also led to significant damage to oil and gas infrastructure. According to the head of the International Energy Agency (IEA) on 23 March, 40 energy assets across nine countries have been severely or very severely affected. While ports, such as Yanbu (Saudi Arabia) and Fujairah (UAE), have compensated for some of the lost export capacity due to the blockade of the Strait of Hormuz, the global oil market has lost about 8% of pre-crisis supply.

There is limited potential for increased output from producers outside the Middle East in 2026, as most operators are constrained by project cycle times, equipment shortages and limited transportation options. Qatar is unable to divert its LNG and QatarEnergy had to declare force majeure on long-term delivery contracts with four countries (South Korea, China, Italy, Belgium). Even if the Strait of Hormuz reopens and the conflict subsides quickly, damages to the infrastructure needed to be repaired and bottlenecks in transport and logistics are likely to keep energy prices elevated for some months.

- Refined oil products and petrochemicals

Roughly 10 to 15% of globally traded refined petroleum products transit through the Strait of Hormuz. As a result, immediate availability of transport fuels (diesel, gasoline and jet fuel), especially in Asia and Sub-Saharan Africa that rely on Gulf refineries, is affected. Even though prices of all types of transport fuels are increasing, diesel and jet fuel are among those that have increased the most.

Asian and Eastern African countries have implemented fuel rationing or export restrictions, securing domestic supply but tightening availability on regional markets. Naphtha shortages have already led Asian plastics producers to declare force majeure as naphtha is the primary petrochemical feedstock in Asia, essential for producing ethylene, propylene and butadiene used in plastics, synthetic textiles and industrial products. With the region’s petrochemical industry heavily reliant on imports from the Middle East, naphtha is crucial for Asia’s vast chemical and manufacturing sectors.

- Fertilisers and agriculture

Global fertilisers production is also expected to be significantly impacted, since 27% of global ammonia exports, 22% of phosphates and 45% of sulphur, which are all essential fertilisers or raw materials for fertiliser production, are exported from the Gulf countries by bulk carriers to reach international markets. Because fertiliser markets operate on just in time logistics and lack strategic stockpiles, prices react faster and more sharply than oil markets.

Roughly one quarter to one third of globally traded nitrogen fertilisers (i.e. ammonia-based urea and ammonium nitrate and sulphate) move through the Strait, meaning even a partial closure immediately tightens supply. Additionally, nitrogen fertiliser production has been affected by plant closures caused by natural gas shortages, since these fertilisers are processed using natural gas.

Sulphur is both a fertiliser in itself and a critical feedstock for sulfuric acid, which is essential for producing phosphate fertilisers. Disruptions have therefore caused immediate shortages and price spikes in sulphur, with knock on effects on phosphate processing worldwide.

Saudi Arabia is a top four global exporter of phosphates, and its exports rely on shipping routes that pass through the Strait of Hormuz. With Chinese phosphate exports already restricted and sulphur supply constrained, the disruption sharply narrows alternative sources, pushing phosphate prices higher.

This raises the cost of DAP (Diammonium phosphate) and MAP (Monoammonium phosphate) fertilisers, widely used for cereals and oilseeds, amplifying global food price risks. The combined disruption of ammonia, sulphur and phosphates creates a fertiliser led inflation shock, which typically feeds into food prices with a lag of a few months.

As farmers have limited short term options for substitution, a prolonged disruption at Hormuz will pose a direct risk to global crop yields and food affordability. Agricultural producers reliant on fertilisers, such as India, Brazil and parts of Southeast Asia, are among the most vulnerable.

- Energy-intensive manufacturing sectors

While crude oil price rise impact is felt worldwide (all crude oil benchmarks have significantly risen), the evolution of gas prices differs across regions. While gas prices have only risen by a few percentage points in the USA, gas prices have considerably increased in Europe and Asia, implying competitiveness issues.

In this context, all energy-intensive sectors are particularly vulnerable. Even if gas price is still well below its 2022 peak, its significant increase will affect the following sectors in Asia and Europe in particular: metals (including steel production); fertilisers; construction materials (such as cement and glass); agriculture; food and beverage; power generation; oil refining; textiles; paper; chemicals (which are already under significant pressure) and the downstream sector: automative; machinery and equipment.

- Aluminium

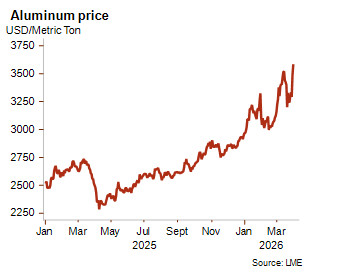

The war in Iran is worsening an already tight aluminium market by triggering production shutdowns across the Middle East, a region that normally accounts for a significant share of global refined aluminium (around 10%). Smelters in countries such as Bahrain, Qatar and the UAE are facing gas supply interruptions and logistical bottlenecks, forcing some plants into controlled shutdowns that could take many months to reverse. The region also depends heavily on uninterrupted shipping for both raw material imports and metal exports, and disruptions to transport, insurance and port access increase the risk that temporary delays evolve into structural shortages. Aluminium prices jumped by more than 5 per cent in early London trading on Monday 30 March, rising above USD 3,450 per tonne and hovering near their highest level in four years, after Iranian missile and drone strikes hit major aluminium production sites in the Gulf over the weekend. The price move reflects growing concerns about prolonged supply disruptions. Emirates Global Aluminium, the region’s largest producer, reported significant damage at its Abu Dhabi facility, while Aluminium Bahrain said it was assessing the extent of the damage to its plant.

Even before the conflict, the aluminium market was already under strain. Exchange warehouse stocks in the US, Europe and Asia are extremely low, while factors such as US tariffs and earlier fears of tighter global supply had already pushed prices higher. The new disruptions therefore worsen an already fragile situation. Another complication comes from China, the world’s largest producer. Despite its dominant position, Chinese output cannot increase freely due to a production cap introduced in 2017. Consequently, rising domestic demand limits China’s ability to compensate for shortages abroad.

The conflict has also triggered panic buying by major industrial consumers, particularly carmakers, amid fears that aluminium supplies could run out within months if disruptions persist. Several Western manufacturers report difficulties in securing new aluminium deliveries and are increasingly drawing down inventories expected to last only a few months and relying more heavily on scrap. Europe and Japan are particularly exposed, as both rely heavily on aluminium imports from the Gulf. Europe sources about 14% of its imports from the region, while Japan depends on it for roughly a quarter. Because car manufacturers must adhere to stringent specifications, it can take as long as 18 months to find new suppliers. If the conflict persists, this situation could lead to production reductions starting in mid-2026.

- Airlines

Airline traffic between Europe and Asia has been significantly affected by the conflict due to the Gulf region’s vital role as a hub in connecting both areas for passengers and cargo.

The sector will be significantly impacted by increasing jet fuel prices and possible fuel shortages if the conflict is not resolved quickly. Airlines in the US and Canada are particularly vulnerable to these fluctuations, as they typically do not engage in fuel cost hedging, unlike many European carriers. Furthermore, adjustments to flight routes to circumvent the Middle East have resulted in longer travel distances and elevated operating expenses.

- Electronics and healthcare devices

Supplies of key computer chips, fibre optic cable or certain medical imaging systems could also be disrupted. Helium is essential for heat management during semiconductor production, and it has no viable alternatives currently. It is only produced in a handful of countries, with Qatar among the leading players in the industry. The situation is particularly concerning given that helium has an extremely short shelf life in its liquid form.

Analysts: Laura Pierssens – l.pierssens@credendo.com, Florence Thiéry – f.thiery@credendo.com