Lithium, cobalt, nickel and copper market update: volatility, supply risks and diverging trends

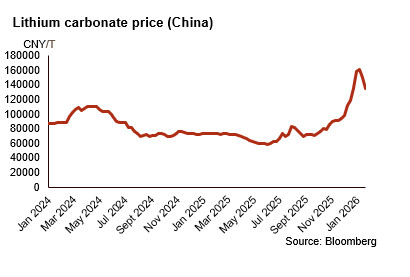

Lithium’s peak of late January gives way to a February pullback

Lithium prices have surged sharply since mid‑December, driven by a combination of Chinese supply concerns and stronger demand expectations for 2026. The rally accelerated after China announced a reduction in VAT export rebates on lithium‑ion batteries from 1 April 2026, prompting producers to front‑load battery production and exports in early 2026. Downstream buyers also restocked before the Chinese Lunar New Year. As a result, lithium carbonate prices in China jumped by 78.3% in just over a month, reaching their highest level since late 2023, before easing slightly. On the supply side, regulatory uncertainty in China adds to market tightness. Local authorities in Yichun plan to cancel several lithium‑related mining permits and the prolonged suspension of CATL’s Jianxiawo mine raises questions about the pace at which supply could recover. While permit cancellations are expected to have limited immediate impact as they mostly concern non‑operational mines, the delayed restart of CATL’s mine is closely watched as a signal of China’s broader approach to lithium supply management.

However, in the first week of February, lithium prices retreated, aligning with the sharp pullback in speculative metals as markets reassessed the outlook for power‑storage demand in major economies (see graph below). The decline was amplified by oversupply concerns, after Chilean exports jumped ahead of the Lunar New Year. Simultaneously, market liquidity diminished as Chinese buyers concluded restocking activities and transportation systems experienced holiday-related slowdowns, while demand, especially from the nickel-cobalt-manganese (NCM) battery sector, continued to be subdued. Overall, sentiment turned cautious, with producers suspending offers and buyers stepping back amid heightened price risks.

China’s increased investment in power grids, data centre infrastructure and large‑scale energy storage is supporting the demand outlook for lithium and other battery metals. Beijing has announced significantly higher spending on battery energy storage systems, aiming to expand installed storage capacity. These initiatives, driven by rising electricity demand from renewables and data centres, are expected to boost demand for lithium‑intensive energy storage solutions.

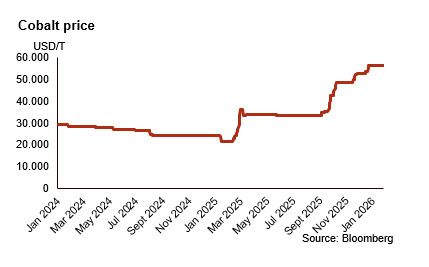

Cobalt prices strengthened in January and have remained stable

Cobalt prices rose in January, mainly due to continued supply disruptions in the Democratic Republic of Congo (DRC). Regulatory crackdowns on artisanal mining temporarily halted processing and delayed shipments. Although the DRC government extended the 2025 export quotas until March 2026 to ease bottlenecks, exports remain irregular and supply is expected to stay tight until shipments normalise. On the demand side, higher prices have not significantly reduced cobalt consumption. Unlike lithium, cobalt demand is more diversified. Strong aircraft deliveries, high defence spending and steady demand from consumer electronics and superalloys are supporting the market. While cobalt use in EV batteries is declining, especially in China, the metal still benefits indirectly from China’s expanding EV partnerships and global supply chain investments, which support broader battery and industrial demand. Since the rise in early January, prices have stabilised, with spot cobalt metal and hydroxide assessments remaining constant as trading activity quietened ahead of the Chinese Lunar New Year.

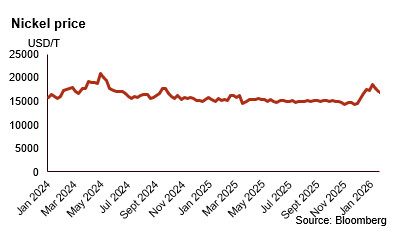

Nickel climbs sharply before adjusting on weaker market sentiment

Nickel prices rebounded sharply in early January after remaining range‑bound in the second half of 2025. The surge in prices was sparked by the news that Indonesia, the biggest global producer of mined and primary nickel, reduced its 2026 nickel ore production quota to 250-260 million metric tonnes, down from 379 million metric tonnes in 2025. This move is part of the Indonesian government’s plan to better balance market supply and demand. The market sentiment was further bolstered when PT Vale Indonesia temporarily halted mining activities due to delays in receiving its annual production permit. These developments triggered a strong speculative reaction, with nickel prices rising by roughly 30% month‑over‑month between 15 December 2025 and 15 January 2026. However, prices began to ease once the Indonesian government authorised PT Vale Indonesia to resume operations, while persistent global oversupply and uncertainty surrounding US trade policy continue to weigh on market fundamentals.

Since the end of January, nickel prices have weakened reflecting softer demand (see graph below). Market sentiment has been subdued, with buyers stepping back and trading volumes thinning as the Chinese Lunar New Year approaches. A stronger US dollar also weighed on prices, reinforcing the downtrend. Rising Shanghai Futures Exchange (SHFE) nickel inventories added to the pressure by signalling softer downstream demand. Speculative positions are currently being scaled back, adding to market volatility and leaving nickel prices exposed to further short‑term corrections until demand strengthens or broader macroeconomic sentiment becomes more stable.

Overall, Indonesia’s quota system remains a major source of market uncertainty. Limited transparency on approved volumes, actual usage and ore quality means that reported quota cuts may not lead to real reductions in nickel supply. This matters for the global market, as Indonesia is a key supplier of nickel ore, especially for electric vehicles and stainless steel.

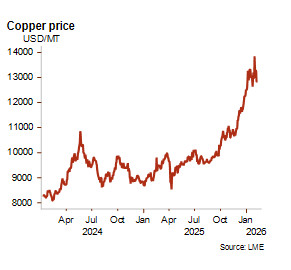

Persistent volatility in the copper market

Copper prices surged at the end of December and reached a new record in early January, mainly driven by speculative inflows linked to rising silver prices. However, they demonstrated notable resilience despite a decline in physical demand, especially in China, where elevated prices have resulted in a significant reduction in new orders and in an increase in inventories. This resilience reflected a combination of factors: expectations of US Federal Reserve rate cuts, tight concentrate availability and continued metal inflows into the US market.

Copper prices have repeatedly reached record levels, exceeding USD 13,000/metric tonne. This indicates a significant transformation in the fundamental attributes of copper as a commodity, with pricing being now influenced not only by traditional industrial cycles but also by global energy transition initiatives and technological advancements. The increase in copper prices reflected both an adjustment for prolonged underinvestment in mining operations worldwide and a reassessment of risks associated with the energy transition and geopolitical factors. Amid high global uncertainty, notably related to the role of the US dollar, copper is more and more seen as a safe haven and its value is increasingly correlated with gold and silver prices.

Copper prices remain highly volatile, alternating between strong rebounds and renewed declines. In early February, the market corrected sharply amid a stronger US dollar and changing expectations around US monetary policy. In China, sentiment weakened ahead of the Lunar New Year, with many buyers stepping back and spot activity slowing. Rising London Metal Exchange (LME) inventories further highlighted softer demand. Although speculative flows briefly lifted prices, particularly following signals that China may expand its strategic reserves, the broader trend remains fragile. Copper trading seems to remain dominated by speculative positioning rather than any clear improvement in underlying fundamentals.

Copper prices are likely to experience considerable fluctuations throughout the year. High copper prices could reduce real consumption and add pressure as stockpiles build up. Should optimism regarding fewer US import tariffs on refined copper continue and Commodity Exchange (COMEX) prices remain lower than LME prices, copper stocks may leave the US, which would help balance the global refined copper market. This situation is expected around mid-year, when increased production from the Kamoa-Kakula and Grasberg mines should also ease tightness in the concentrated market.

Analyst: Laura Pierssens – l.pierssens@credendo.com