Philippines: Political fragmentation, heightened public defiance and geopolitical risks might weigh on the 2026 outlook

Event

The Philippines’ GDP growth slowed to 4.4% in 2025, a five-year low. This year’s rebound to 5.3%, announced by the IMF, is uncertain given the deteriorated external environment with high geopolitical risks and the impact of the US trade war. Even more importantly, the economy is harmed by domestic headwinds. The country was not only hit by an extreme typhoon last November, highlighting high exposure to climate shocks, but also continues to experience serious political instability, hitting consumer and investor confidence and government policies. Political instability first began in March 2025 with the arrest of former President Rodrigo Duterte and his transfer to the ICC in The Hague, amplifying polarisation between the Marcos and Duterte political dynasties. Later in the year, a major corruption scandal broke out around the irregular use of funds related to government flood control projects, leading to mass protests. In response, President Marcos Jr. has committed to tighten anti-graft measures and scrutiny in public spending. More recently, an impeachment procedure against Marcos Jr. has been submitted to the House of Representatives, though it has a low probability to succeed. Despite popular pressures and active political opposition, Marcos Jr. can rely on the backing of the army and his core supporters. Political fragmentation and strained relations between Marcos Jr. (who is not allowed to run for a second mandate) and his deputy Sara Duterte – daughter of Rodrigo Duterte – will nevertheless continue to weigh on domestic stability and business sentiment until 2028, when the next presidential elections will be held.

Impact

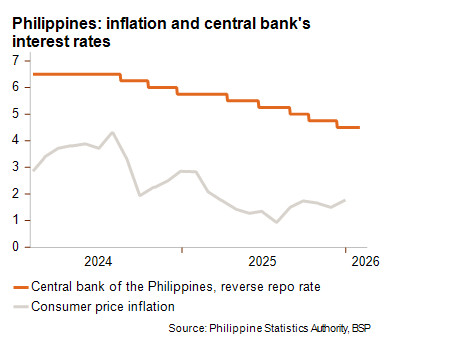

The Philippines’ economic deceleration amid the high-profile corruption scandal has also been reflected by the peso fluctuating at historically low levels vis-à-vis the US dollar. Hence, slowing growth and contained inflation have led the central bank to continue its loosening policy and it has made several policy rate cuts in 2025 (from 5.75% to 4.5%).

Looking ahead, monetary support combined with a strong services sector, remittances, a potential stabilisation in consumer demand and increased fiscal spending could help boost the economic activity this year. Ongoing export market diversification, leading to talks about free trade agreements with partners outside Asia (e.g. a concluded agreement with the UAE, ongoing negotiations with the EU), driven by a more uncertain and transactional US partner (the US is the country’s first export market of goods and a key security ally), should also play a supportive role in the future. Downside risks for this year will be dominated by an unstable domestic political climate, uncertain global economic developments and persisting elevated maritime tensions with China in contested areas in the South China Sea. Although the Philippines’ chairmanship of ASEAN this year might highlight the country’s regional profile and provide some political benefits internally, it is unlikely to ease long-standing maritime disputes.

The country risk ratings are expected to remain unchanged in the coming months.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com