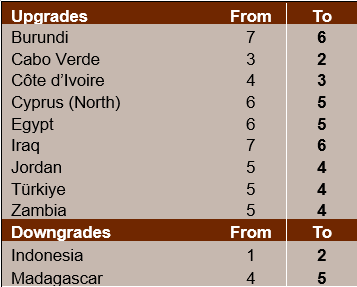

Short-term political risk: Nine countries upgraded, two countries downgraded

In the framework of its regular review of short-term (ST) political risk, Credendo has upgraded nine countries and downgraded two countries.

- Burundi: upgrade from 7/7 to 6/7

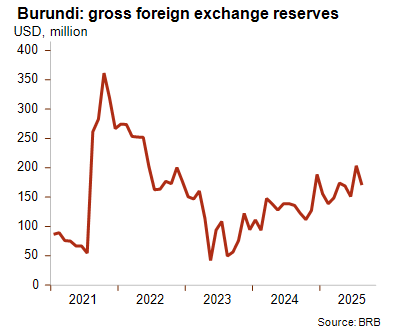

While foreign exchange levels remain low, covering less than 1.5 months of imports, the situation has markedly improved from the levels of 2023, as can be seen in the graph below. This improvement is likely supported by Burundi’s peg to the US dollar, since the recent weakness of the dollar has reduced the need for costly interventions on the foreign exchange market. The current account balance has also improved significantly over the last couple of years, though it remains deeply negative with a deficit of around 8% of GDP.

The last time Burundi was upgraded, in September 2022, the main driver was a large increase in foreign exchange reserves, which was prompted by a disbursement from the Rapid Credit Facility of the IMF. This disbursement was used up over the course of the next year and a half, leading to a downgrade in December 2023. This time, the improvement does not rely on a one-off inflow, which means it might be more robust and justify a rating upgrade to 6/7 – though Burundi remains vulnerable to external shocks.

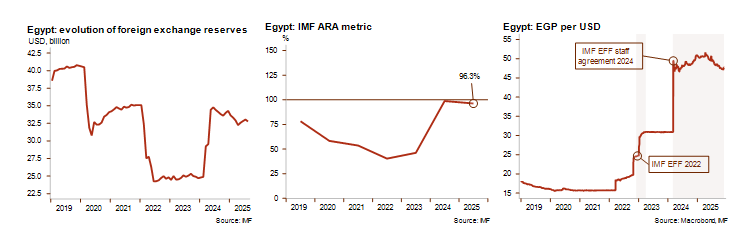

- Egypt: upgrade from 6/7 to 5/7

The acute liquidity pressures Egypt was experiencing in 2022-23 have alleviated thanks to lower commodity price pressures, strong remittances and tourism sector performance, and external support from regional partners (such as the UAE and the EU) and multilaterals (such as the IMF and the World Bank). In this context, foreign exchange reserves have recovered and are assessed as broadly adequate. Therefore, the ST political risk rating has been upgraded to 5/7. Moreover, authorities have implemented key reforms to stabilise the macroeconomic situation, such as the shift to a more flexible exchange rate regime.

In this context, Egypt is showing signs of macroeconomic stabilisation, with inflation lower than in the past two years – albeit still high – and growth accelerating. Nonetheless, the country is not out of the woods as key risks remain in the short term amid erratic global trade policies and geopolitical risks, in particular the fallouts from the instability in neighbouring Sudan and Gaza. While the Houthis’ alleged decision to suspend disruptions to Red Sea maritime traffic is a very positive development for Egypt as it could restore Suez Canal revenues, the risk of renewed attacks in the near term remains high. In fact, the suspension is conditional to Israel respecting the ceasefire in Gaza, which is already under strain. Moreover, Egypt is very vulnerable to fallouts from tensions between Iran and Israel. As the country relies on gas import from Israel, any renewed escalation could once again disrupt gas inflows and trigger capital outflows, as reportedly happened during the 12-day war between Iran and Israel.

- Iraq: upgrade from 7/7 to 6/7

The upgrade to 6/7 has been implemented on the back of easing security risks. Iraq has been able to maintain a relative political stability despite heightened regional tensions and initial concerns of the country’s possible engulfment in the confrontations between Iran and Israel. The government led by Prime Minister al-Sudani has so far succeeded in carefully balancing pressures by both Iran and the US. Reflecting the country’s improved security environment, the November parliamentary elections were held at relative calm, given Iraq’s historical standards.

Despite the improvement in Iraq’s security situation, political violence risks remain important.

While current authorities have managed to balance pressures between Iran and the US, it is unclear at this stage if the next government will prove capable of maintaining this difficult balance. If this is not the case, the country could for instance be exposed to renewed instability and repercussions from the Trump administration’s “maximum pressure” campaign on Iran because it would be targeted by more severe US sanctions. Additionally, given Iraq’s political environment, government negotiations tend to be contentious and the risk of flare-ups of violence can therefore not be excluded during the ongoing government formation negotiations.

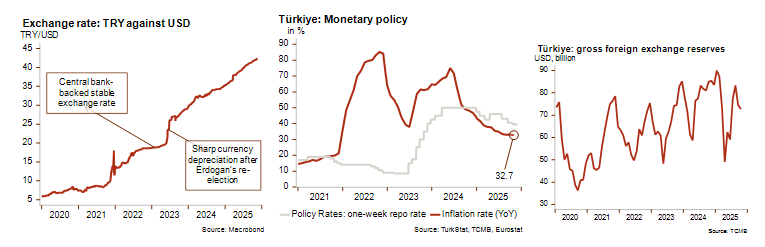

- Türkiye: upgrade from 5/7 to 4/7

The upgrade of Türkiye’s short-term political risk rating has been driven by markedly improved external liquidity and access to financial markets. Furthermore, following his re-election in May 2023, President Erdoğan appointed a more orthodox economic team, led by Finance Minister Mehmet Şimşek. Despite several changes in central bank leadership, the monetary policy has become more conventional. As shown in the graphs, the central bank has raised its benchmark interest rates, which permitted the Turkish lira to depreciate, and it has also withdrawn certain unorthodox financial instruments. These policy changes have led to a sharp depreciation of the Turkish lira, which has intensified inflationary pressures. Nevertheless, these measures have contributed to a gradual reduction in macroeconomic imbalances, including a narrowing of the current account deficit and a sustained decline in inflation, although inflation remained high at 32.7% in October.

Foreign investor sentiment has improved significantly, enhancing Türkiye’s access to global financial markets. This is particularly notable given the country’s continued reliance on portfolio flows to finance its (now reduced) current account deficit, despite a marked decrease in dependency. However, any deterioration in foreign investor confidence – as seen in March 2025 following the arrest of Istanbul Mayor Ekrem İmamoğlu – can lead to substantial capital outflows and a sharp reduction in gross foreign exchange reserves. Although the latter have partially recovered since then, they remain volatile. Moreover, the exchange rate continues to depreciate. This said, those factors were no obstacle to an upgrade, given the country’s very strong macroeconomic fundamentals, namely a low public and external debt, and a large, diversified and resilient economy.