Short-term political risk : Three countries upgraded, five downgraded

In the framework of its regular review of short-term (ST) political risk, Credendo has upgraded three countries and downgraded five countries.

- Botswana: downgrade from 1/7 to 2/7

A diamond market contraction since 2022 translated into a drop in global diamond demand and prices. As diamond exports make up 86% of Botswana’s export revenues, the current account deficit widened substantially in 2024 and foreign exchange reserves fell by about 30%. A shift in consumer preference towards cheaper lab-grown diamonds is the main driver behind the crisis. However, Trump’s trade tariffs have further worsened prospects as about 12% of Botswana’s total goods exports are directed to the US market. This is expected to result in a second consecutive year of economic contraction in 2025. Nevertheless, the country’s large liquidity buffers, together with strong governance and policymaking credentials, a sound financial sector, solid institutions and a stable political climate are essential building blocks that should enable Botswana to cope with the today’s headwinds. In fact, Botswana remains among the best classified countries in the region despite the downgrade to ST political risk category 2/7.

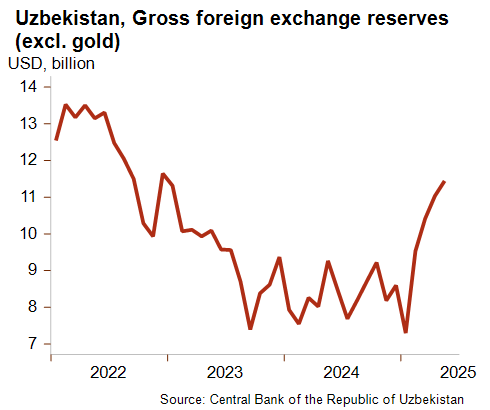

- Uzbekistan: upgrade from 4/7 to 3/7

Liquidity has been sharply improving this year on the back of surging foreign exchange reserves excluding gold (+56% between January and May 2025), while the ST external debt remains relatively low. As a result and boosted by rising exports of food and gold but also by strengthening tourism receipts and workers’ remittances, foreign exchange reserves are nearing the adequate import cover threshold of three months. Moreover, they are now easily exceeding the moderate external debt service scheduled for this year. It is also worth stressing that Uzbekistan’s liquidity position is reinforced by a potential buffer offered by its sovereign wealth fund (equivalent to 5% of GDP) and large gold reserve (USD 37.7 billion in May 2025). Despite the global economic slowdown, Uzbekistan keeps a strong ST economic outlook, supported by rising FDI plans in multiple projects (transport infrastructures, critical minerals, renewables, climate-related) which are attracted by a reformist government and a high growth potential. More generally, Uzbekistan’s improving political risks reflect a positive economic and trade momentum in Central Asia.

- Vietnam: downgrade from 2/7 to 3/7

The country’s liquidity position has been slowly weakening since May 2024 and has seen further erosion this year as reflected by the decline in foreign exchange reserves. This is happening in a context of trade turmoil triggered by the announcement of high US import tariff rates which cloud the global economic outlook. Vietnam is particularly at risk given its high economic openness, integration in global supply chains and exposure to the US market. Hence, Vietnam’s exports and FDI inflows could be hit hard, thereby increasing pressures on its foreign exchange reserves. Those adverse developments and deteriorated economic prospects explain the downgrade from 2/7 to 3/7.