Angola: Investment efforts aim for vital economic diversification

Highlights

- While Angola’s economy still depends largely on hydrocarbons, growth is increasingly propelled by non-oil sectors.

- Liquidity has stabilised despite exposure to oil market volatility, and inflation has begun a steady downward trend.

- Angola’s external debt position benefited from debt management reforms and more prudent borrowing decisions, though it still faces a significant debt servicing burden.

- To achieve a sustainable outlook, progress in economic diversification will be vital.

Pros

Cons

Head of State

Description of the electoral system

Population

GDP per capita

Income group

Main export products

Encouraging economic prospects that are increasingly steered by non-oil sectors

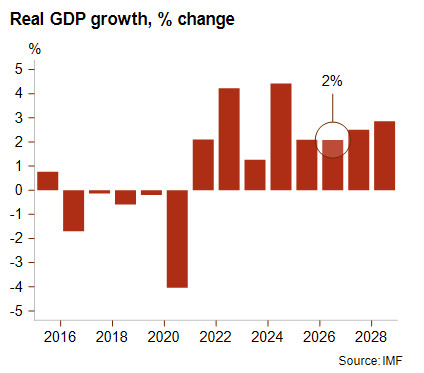

Since 2021, GDP growth in Angola has rebounded following five years of recession and is forecast to reach between 2% and 3% in the coming years. While the economy remains highly dependent on hydrocarbons, non-oil sectors – including agriculture, information and communications technology, manufacturing and public infrastructure projects – are driving economic activity. Angola has been gradually pursuing economic reforms since President Lourenço took office in 2017, yet declining oil production has highlighted an urgent need for advanced economic diversification in the near term.

Angola’s investment drive is mainly focussed on agriculture, mining and infrastructure and logistics linked to the Lobito corridor. The latter has been backed by US and EU financing, highlighting Angola’s increased strategic value for the West while China’s dominance as Angola’s primary lender has been decreasing. The corridor connects the Congolese and Zambian copper belt to the port of Lobito, building on Angola’s role as a regional logistics hub while providing transport potential to broader sectors over time. The mining sector (gold, iron ore, copper, uranium, lithium, etc.) holds key potential and is likely to attract more investor attention in time.

Angola continues to be a prominent diamond exporter, yet the recent slump in the natural diamond market in favour of lab-grown diamonds has blurred projections: to find out more, please refer to this article on the diamond crisis. The anticipated Angolan and Botswanan acquisition bid for De Beers aligns with the country’s intention to raise domestic diamond production over the coming years. Meanwhile, the energy sector is also attracting greater investments once more in refinery capacity and hydrocarbon production rehabilitation. Another part of the investment drive involves the privatisation of some prominent state-owned enterprises – such as the oil company Sonangol, which is looking to sell a 30% stake, and the telecoms company Unitel – which is expected to take speed as of 2026.

Inflation has embarked on a gradual declining path

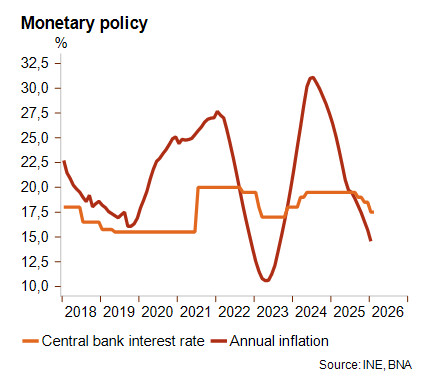

For over a decade, Angola has persistently struggled with high levels of inflation. Since its peak in mid-2024 at 31%, inflation pressure has decreased continuously and dropped down to 14.6% in January 2026. This gradual decline in inflation is projected to continue, and the IMF expects it to reach 10% by 2027, thanks to tighter monetary policies and foreign exchange market reforms.

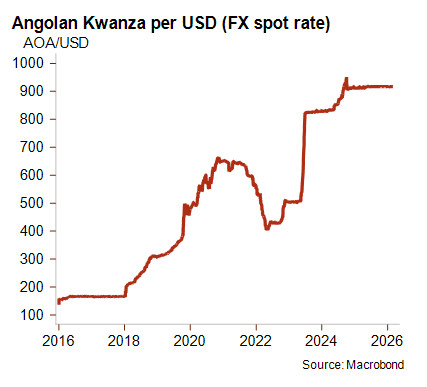

During the IMF financial support programme of 2018–2021, the government committed to the implementation of various critical reforms, including VAT implementation, a more floating exchange rate, a privatisation scheme and the gradual elimination of fuel subsidies. Following the introduction of a more flexible exchange regime, the kwanza sharply depreciated and oil market fluctuations caused episodes of volatility, leading to soaring external debt services in local currency terms and inflationary pressure. The Banco Nacional de Angola (BNA) is now intervening on a managed-float basis to smooth kwanza volatility in times of falling oil revenues.

Liquidity levels remain predominantly reliant on the hydrocarbon sector

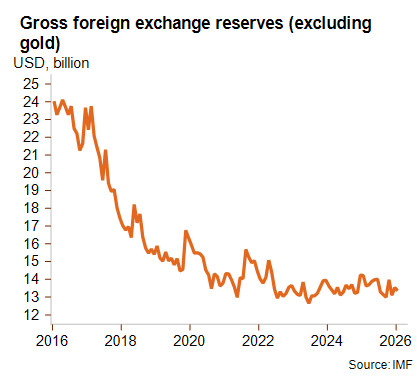

For the most part, Angola’s liquidity position continues to rely on hydrocarbon export revenues, accounting for more than 95% of foreign exchange revenues and rationalising Angola’s extreme vulnerability to oil market instability. The risk of price volatility in combination with falling domestic production directly affect liquidity, destabilising the exchange rate and affecting the external debt servicing burden quite drastically, as witnessed during different episodes over the past decade. The recent surge in global energy prices resulting from the war in the Middle East will support export revenues in the near term.

Following the oil price drop in 2015–2016 and the sharp fall in crude oil production levels between 2015 and 2021, foreign exchange reserves trended down continuously. However, a rough stabilisation in oil production since 2021 has led to recovering USD inflows, stabilising reserves for a solid six months of import cover since 2024. Despite current account surpluses that are essentially structural, certain foreign exchange controls are maintained by the BNA to protect its liquidity position, as volatile investment inflows and capital flight periodically leave financing gaps on the external balance, squeezing the availability of hard currency in the market. Other elements explaining persistent pressure on reserves are related to the fact that Angola is an import-dependent economy as a result of an underperforming non-oil economy. Angola’s agricultural sector, for example, is underperforming, largely because it never recovered from the destruction and disruption caused by the civil war (1975–2002). Extensive investments currently underway, however, could unlock significant latent potential.

Despite substantial debt servicing pressure, Angola’s public debt position is improving

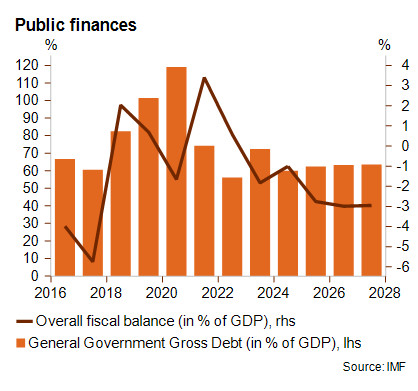

Public finances have seen remarkable improvements over the past few years. Gross government debt came down to 63% of GDP in 2025 from its peak during the Covid-19 period following cycles of deep kwanza depreciation, with more than 90% of the debt as foreign currency-denominated debt. The fiscal deficit is estimated to balance around a healthy 3% of GDP over the coming years, keeping the debt stock relatively stable. Nevertheless, financing pressure remains elevated, as interest payments on public debt alone are expected to absorb a third of government revenues in the years ahead. The 2026 budget does include meaningful expenditure adjustments to help preserve stability while further fuel subsidy cuts were postponed following civil unrest in July 2025. The US and Israeli military campaign against Iran begun in February is likely to mark the beginning of a substantial surge in international energy prices, which will benefit Angola’s fiscal revenues at least in the near term.

When considering Angola’s external debt position, it is fair to say that it has improved substantially since 2022 thanks to more prudent borrowing decisions and debt management reforms. Angola has increased creditor diversification and moved away from its overreliance on Chinese (collateralised) debt, and has re-engaged with the international capital markets through its Eurobond issuance in October 2025. Nevertheless, large external debt services due in 2026 and 2027 are still set to raise debt sustainability risks and add pressure to liquidity.

Pronounced risks to Angola’s macroeconomic stability prevail

The most important immediate risk for Angola’s macroeconomic stability stems from its over-reliance on hydrocarbon export revenues, exposing it to oil sector shocks. To sustain debt sustainability over time, progress in economic diversification is therefore critical, together with retained prudent borrowing. Political instability risks have lowered since President João Lourenço took office in 2017, leading the country into the post-Dos Santos era by seeking to reverse decades of patronage and governance failures while pursuing market-oriented reforms. Nevertheless, the high cost of living – combined with the dismantling of fuel subsidies, rising education fees and general weak socioeconomic conditions – has triggered civil anger and led to deadly protests in July 2025. In fact, President Lourenço’s ruling party, the People’s Movement for the Liberation of Angola (MPLA), is becoming increasingly unpopular in the run-up to sensitive presidential elections due in 2027. Therefore, the risk of political unrest might further increase over the coming year. Angola is also highly exposed to climate-related shocks, in particular severe droughts, erratic rainfall and prolonged dry spells, leading to crop failures and rising food insecurity. Angola is classified in category 6/7 for medium-to-long-term political risk and prospects will depend predominantly on a reduction in hydrocarbon reliance and the stabilisation of debt servicing pressure.

Analyst: Louise Van Cauwenbergh, l.vancauwenbergh@credendo.com