Main challenges facing Sub-Saharan Africa in 2026 and beyond

Highlights

- Favourable terms of trade, lower inflation, strong GDP growth and recovering liquidity levels emphasise Sub-Saharan African resilience amid tough global conditions.

- Erratic US trade policies are accelerating the transformation of trade orientation in the region.

- The continent could take advantage of geopolitical rivalry over high-value commodities when trade shifts beyond raw extraction.

- Besides intensifying climate shocks, violent conflict and high debt sustainability risks drive the region’s risk outlook.

Improved terms of trade and a weaker US dollar support performance

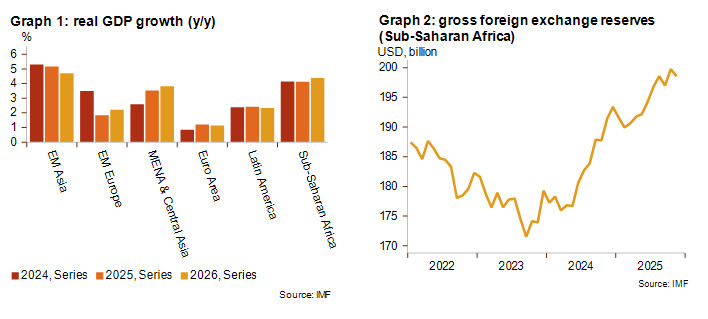

Talking about Sub-Saharan Africa as a single unit is somewhat tricky given the enormous heterogeneity across countries, but there are some general trends that can be identified. Despite the challenging global environment, momentum for economic growth in Sub-Saharan Africa remains strong compared to other regions in the world (graph 1), underpinned by improved terms of trade and declining inflation. In addition, African exchange rates have been stabilising over the past six months, assisted by a weaker US dollar, which is also helping to cut debt service payments and ease inflation. Graph 2 shows that liquidity levels have been recovering in Sub-Saharan Africa since 2024, supported by regained access to Eurobond financing by some countries (Kenya, Côte d’Ivoire, Senegal, Gabon, Nigeria, Egypt, Benin and Angola) and favourable commodity price trends. In 2026, commodity exporters with diversified baskets are most likely to show the most resilience in terms of liquidity.

Unreliable US trade policy towards Africa will accelerate shift in trade relations

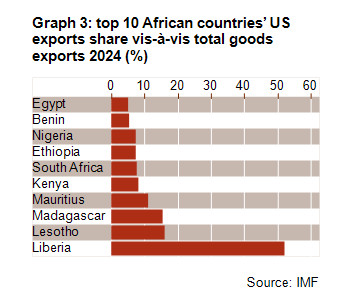

Africa is not highly exposed to Trump’s raging trade war, as only a few countries export large values to the USA (Graph 3). Markets such as Liberia, Lesotho and Madagascar have been on high alert since Trump took office for the second time. The USA’s disengagement from African trade was displayed by the expiry of the 25-year-old African Growth and Opportunities Act (AGOA) in September 2025, which gave most African countries duty-free access to the US market. AGOA only represented 1% of Africa’s total export volume, but it mainly concerned labour-intensive sectors such as textiles, leading to social tensions over mass layoffs and rising unemployment levels. China anticipated by filling the void and introducing a comprehensive zero-tariff trade pact with the region last summer. It is also expected that, besides altering external trade and investment partnerships, growing regional integration will also transform Africa’s trade geography at a fast pace. In fact, trade reorientation between African states has already been accelerated by means of the African Continental Free Trade Area (AfCFTA), promising great potential in the longer term.

On 3 February, President Trump signed a one-year extension of AGOA after Congress continued to pursue the issue following its September 2025 expiry. However, Trump’s wider tariffs scheme supersedes AGOA, meaning the one-year extension will only ease tariff pressure on goods exports that are exempted from the tariff list. This episode once again underscores the carelessness and volatility characterising recent US trade policy in Africa. The AGOA extension moreover carries a high risk of political weaponisation, as certain countries could once again be excluded from the agreement due to bilateral disputes with the US administration, often linked to domestic political issues rather than trade. This was witnessed in past tensions with South Africa and Nigeria.

Commodity-driven trade holds potential when transformed beyond old exploitative patterns

In the past, Africa’s natural riches have not translated into widespread peace and prosperity – on the contrary. This continues to be a major challenge for the region holding roughly 30% of the world’s critical minerals such as cobalt, lithium, copper and rare earth elements. African trade will be increasingly dominated by the fierce geopolitical rivalry over access to these high-value commodities, which will raise its dependency on non-manufactured exports and defy longstanding diversification efforts for greater added value and economic development. Higher-commodity dependency exposes African countries to shocks related to price volatility, environmental degradation, corruption and social unrest, but on the upside, if managed well, rising export and fiscal revenues could strengthen the economic and financial fundamentals and enhance debt sustainability in the region. Therefore, complementary investments in local processing and value addition remain vital for the region to industrialise and create jobs using its own resources. Finding a sustainable way forwards beyond raw resource extraction will be a key mission for Africa and its partners. Recent large mining investments are showing mixed results, with Mozambique’s LNG mega-project looking like a textbook case of everything that can go wrong, while in Namibia, however, a commodity investment drive is creating encouraging prospects.

African mining is dominated by China, not only in terms of extraction but also in processing capacity and related infrastructure. While the USA has sought to counter China’s growing influence on the continent, recent policy choices – most notably the dismantling of USAID and AGOA and increased travel restrictions – have been perceived as disengagement from Africa. Rather than strengthening US influence, these measures have undermined US soft power, while other players like Russia, Türkiye and the Gulf States have continued to deepen their investment ties across the continent. Europe is also using its Global Gateway strategy to raise strategic influence in the region and to secure diversified access to critical minerals by investing in numerous corridors and enhancing ties.

The search for new funding beyond scrutinised foreign aid, while avoiding the debt trap

Over the course of 2025, it quickly became apparent that the impact of USAID cuts was much more severe for Sub-Saharan Africa than Trump’s trade tariffs. This high reliance on official transfers is considered a serious economic vulnerability, especially when it is vital for financing imports of essential goods. The global trend of cutting foreign aid and waning international solidarity is therefore particularly dramatic for the most fragile countries, such as Malawi, Ethiopia, Burundi, Niger, Liberia, Sudan and Somalia, where the result is that critical services are disrupted with grave humanitarian consequences. Squeezed funding raises the already high risk for a balance of payments crisis and a sovereign default or public debt restructuring.

The less vulnerable countries, on the other hand, are seeking to reallocate budgetary resources and increase domestic and international debt issuances to cover the loss in funding. Some leaders consider this to be positive momentum for a new African self-reliance strategy, but despite the obvious value behind this vision, a key point of focus will be to not replace aid dependency with a debt trap. At present, 21 low-income countries in Sub-Saharan Africa are already at ‘high risk of debt distress’ or ‘in debt distress’ according to the IMF’s Debt Sustainability Analysis, and therefore debt sustainability is considered a major risk in the near term. This will be the focus of an upcoming follow-up publication by Credendo.

Democratic decay fuelling the Gen-Z protest movement

For some years now, Africa has been experiencing a shift towards more autocratic forms of government – a trend that goes hand in hand with weak institutions and that represents a shift away from post-Cold War democratisation efforts. The prevalence of ‘life presidents’, military putschists blocking the transfer to civil rule, electoral manipulation to force incumbent successions and the use of authoritarian political tactics (like running for an unconstitutional additional presidential term), are becoming increasingly embedded.

This partially explains the strong mobilisation of Gen-Z protests across Africa, where youthful populations without economic opportunities confront the old-guard elites through their message that politics is a social contract, not a licence to loot. These are inclusive and leaderless movements, which make them harder to suppress, but increases the risk for exploitation by military or populist leaders who might try to fill the vacuum and seize power – as seen in Madagascar and Burkina Faso. In sharing the same grievances over unemployment, a lack of democratic representation and deficient basic services, pan-African solidarity is growing and could cause a ripple effect across the region, especially given that Africa’s fast-growing population, projected to reach nearly 2.5 billion by 2050, adds pressure on governments to deliver jobs and services to an expanding youth cohort.

The vast challenge of tackling climate change

The incidence and intensity of climate shocks in Sub-Saharan Africa is rising. Therefore, climate change is another leading challenge for the region, along with violent conflicts and public debt vulnerability. The latest El Niño led to the worst drought in Southern Africa in at least two decades, leading to record low water levels, a sharp drop in food production and prolonged power cuts. This has been followed by exceptionally heavy rains, leading to deadly flooding across the entire region. East Africa has also seen extreme rains, where coastal cyclones are hitting areas that have rarely been struck before. Millions in Central and West Africa are affected by floods, while the area is still also seeing episodes of abnormal dryness. The impact of climate shocks such as recurrent heat waves, floods and droughts across the continent on agricultural production, energy supply and logistics are causing supply shortages and raising food imports and inflationary pressure, while the humanitarian impact is leading to social unrest.

Policy priorities to tackle the acute environmental stress include scaling up climate-smart agriculture, strengthening energy systems and reinforcing early-warning and emergency response systems, while providing targeted safety nets for the most vulnerable households. However, the lack of fiscal space and scattered conflicts complicate the implementation of mitigating strategies, while these climate shocks are becoming an increasingly significant source of conflict. The challenge for the region is colossal.

Credendo’s medium-to-long-term political risk classifications keep the score

The aforementioned challenges outline some general trends that can help to navigate through Africa’s risk outlook. When considering the high-risk countries in category 6/7 or 7/7 according to Credendo’s MLT political risk classification, violent conflict is by far the most destabilising long-term risk element. In Sub-Saharan Africa, some conflicts have been raging for years, even decades, making countries economically inaccessible (such as Eritrea, the Central African Republic, Somalia, South Sudan and Sudan). In other countries, economic mismanagement, negligible export returns, capital controls or bad payment morality – often interrelated with grave institutional weaknesses – drive the risk profile. A high probability for sovereign default or debt restructuring, not to mention an actual default-situation, can also explain the high-risk classifications.

Analyst: Louise Van Cauwenbergh (l.vancauwenbergh@credendo.com)