Namibia: Medium- to long-term political risk upgraded to category 5/7

Highlights

- Namibia has a stable political climate and is praised for its ambitious policy-making and strong institutions compared to its regional peers.

- An ambitious economic diversification plan should help to tackle the negative impact of the diamond sector downturn.

- The country’s external debt position is considered sustainable and public finances have been recovering since 2023, leaning on increased domestic financing.

- Despite challenges linked to climate change vulnerability and global trade uncertainties, the outlook is positive, assuming that reform implementation is sustained and social grievances are addressed.

Pros

Cons

Head of State

Description of electoral system

Population

GDP per capita

Income group

Main export products

Economic recovery is supported by stable politics and strong policy performance

Between 2015 and 2020, Namibia was negatively impacted by global commodity shocks and a weakened financial position. Yet over the past three years, ambitious reforms have put the country back on a positive track, while the outlook is supported by large investments. Since 2023, Namibia’s economic recovery has been largely driven by investments in critical minerals (especially uranium and lithium), hydrocarbons, manufacturing and tourism. It is one of the few African upper-middle income countries – largely explained by its natural riches and small population of 3 million – and has strong institutions compared to its regional peers. Furthermore, the stable political climate and solid policy implementation have served to support investor confidence in the country.

The political scene is still dominated by SWAPO (South West Africa People's Organisation), in power since Namibia’s independence from South Africa in 1990 (after German colonial rule ended in 1915, it became an administrative territory of South Africa under apartheid law). However, corruption concerns, high unemployment levels and economic hardship have led to a downward trend in popular support for the ruling party. Nonetheless, SWAPO managed to secure a parliamentary majority during the 2024 general elections, with party leader Netumbo Nandi-Ndaitwah becoming Namibia’s first female president following her inauguration in March 2025.

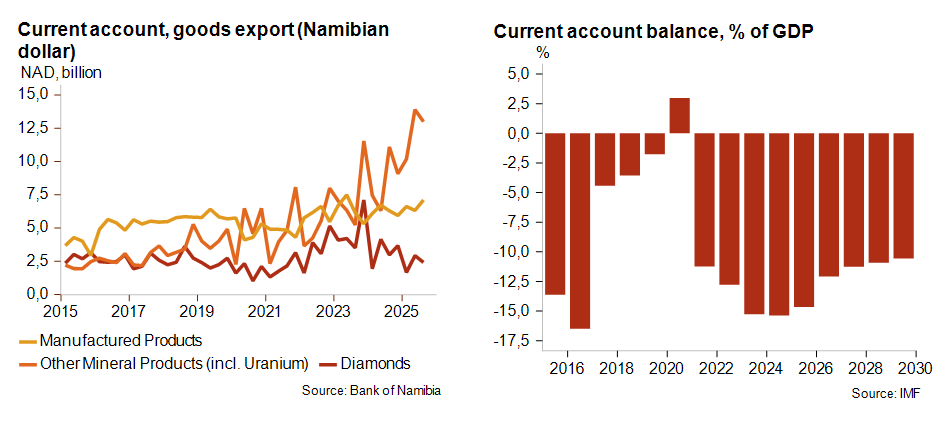

Ambitious diversification plan should help to tackle the diamond sector downturn

Namibia has been feeling the burn of a structural downturn in the diamond sector due to a global shift in consumer preference towards cheaper, lab-grown diamonds. As diamond exports accounted for 10% of current account revenues in 2024, an ambitious diversification plan should break the fall. In 2025, high gold and uranium returns offset the loss, and in the longer term, offshore oil and gas discoveries should provide additional revenues, although this is not expected before 2030. In the meantime, investments related to economic diversification are creating substantial current account deficits, estimated at 12% of GDP in 2026 – including SACU (Southern African Customs Union) revenues – largely financed by FDI inflows. Incoming export returns should narrow the current account deficit, but the realisation of new revenues will be slow. Meanwhile, despite a recent dip, Namibia’s liquidity buffer still sits at an adequate level, with foreign exchange reserves reaching about 3.3 months of import cover in October 2025. This is projected to accumulate steadily over the coming years.

A sustainable external financial position for Namibia

Eurobond issuances in 2011 and 2015 and private foreign direct investment debt raised debt-creating capital inflows on the balance of payments, adding to the upward pressure on Namibia’s external debt witnessed between 2012 (37% of GDP) and its peak in 2020 at 78% of GDP. Ever since, external debt to GDP moderated down to an estimated 68% in 2025, and this should continue on a solid downward track over the coming years. These debts mainly consist of private-sector debt, bearing in mind that Namibia’s public sector external debt only amounts to 14.7% of GDP (2024) – a low level by international standards. Large external debt services used to be a key weakness, but ratios have moderated substantially.

Fiscal consolidation stabilises public finance indicators

Public finances started to improve in 2023, with a return to surpluses on the primary fiscal balance thanks to strong debt management and fiscal prudence. The overall fiscal deficit is projected at -5% of GDP in 2026 and should reach an annual -4% as at 2027, while gross public debt stock peaked at 70% of GDP in 2021 and has been gradually narrowing down to 64% in 2025. This is set to remain stable in the years ahead. Only about 20% of public debt stock is external government debt, meaning that the Namibian government is highly reliant on domestic financing, and while deep domestic capital markets are an important risk mitigator and lower the rollover risk, the government’s high exposure to relatively expensive domestic debt leads to substantial interest costs, and accounted for an estimated 15% of public revenue in 2025. In October 2025, Namibia successfully settled the 2015 USD 750 million Eurobond, further shifting from external to domestic debt instruments.

Worth 11.8% of GDP in 2024, SACU revenues are official transfers and an important source of revenues for Namibia. Falling commodity prices and global trade tensions have been reducing the SACU revenue pool, which could raise fiscal pressure and increase the need for additional borrowing in the short term. However, the IMF considers Namibia’s external and public debt levels to be sustainable, although they have emphasised the need for sustained fiscal discipline.

A positive outlook faced with some key risks

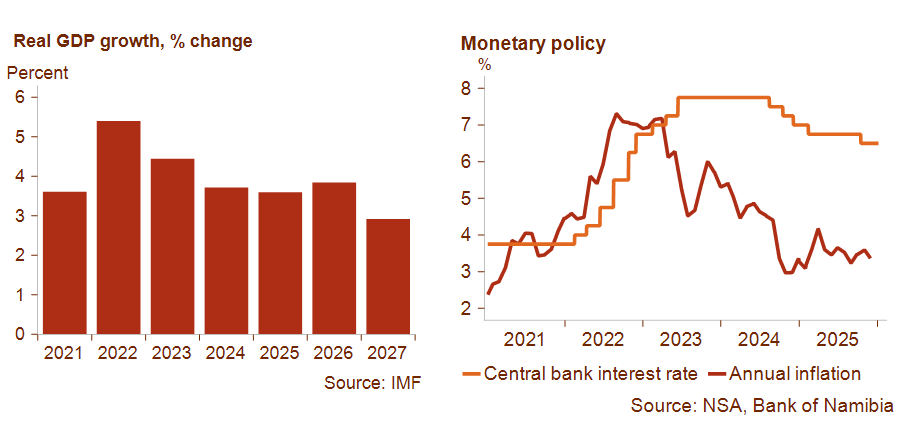

Economic growth is expected to reach 3.8% in 2026 and a solid 3% over the coming years, while inflation moderated again to 3.7% by year-end 2025, down from its 2022 peak. As a result of lower price pressures, the central bank has already lowered the policy rate a few times, which should support economic activity in general. Large, diversified investments are creating encouraging economic prospects, while political stability and strong policy performance are serving to support investor confidence. Since early 2024, the Namibian dollar has strengthened after a decade in which it lost nearly half its value against the US dollar, largely reflecting the volatility and long‑term depreciation of the South African rand, to which it is pegged. The existence of a credible currency peg to the South African rand, however, is considered an important anchor of stability. At the end of 2025, Credendo decided to upgrade Namibia’s medium-to-long-term political risk classification from category 6/7 to 5/7, while the short-term political risk classification has remained stable in category 3/7 for over a decade.

On the downside, Namibia is one of the driest countries in Sub-Saharan Africa, making it highly vulnerable to rising temperatures, erratic rainfall and frequent droughts that threaten agricultural production, water security and livelihoods. Severe drought conditions in 2024 and 2025 depleted herd sizes, affecting the export of live cattle in 2025, and climate change-related shocks like these pose a significant risk not only to the country itself, but the entire region. The country’s investment drive might be overly concentrated on the hydrocarbon sector, exposing it to oil market volatility and environmental degradation risks that could also stir social tensions. In addition, high unemployment, poverty and housing shortages are a persistent source of discontent among the population, while high global trade policy tensions and geopolitical fragmentation create additional challenges to the nation’s outlook. Nevertheless, Namibia continues to be a beacon of stability in Sub-Saharan Africa, a region struggling with high risks of conflict, democratic decay and debt vulnerability, among several other issues.

Analyst: Louise Van Cauwenbergh – l.vancauwenbergh@credendo.com