Energy crossroads: Where is the USA headed?

Highlights

- US solar and wind energy developers face a perfect storm of policy and business environment challenges.

- Other clean energy segments are faring better, notably thanks to surging power demand related to data centres, encouraging innovation.

- However, fossil fuels are still expected to power more than 50% of data centre capacity in the USA by 2030.

- Renewable energy deployment also offers a solution to curb rising US electricity prices.

US wind and solar energy developers face a more adverse climate

On his first day as president, Donald Trump issued an executive order halting new approvals for wind farms. A few months later, his "One Big Beautiful Bill" (OBBB), signed last July, phased out some of the key tax credits for solar and wind projects much sooner than what had been decided under the Inflation Reduction Act in 2022. Eligibility for these projects now requires either starting construction before 4 July 2026 or completion by the end of 2027. Meanwhile, other offshore wind projects that had already secured permits and begun development have also suffered a severe blow from the use of the executive power to revoke them.

In addition to those measures hurting solar and wind projects directly, the OBBB proposes the elimination of electric vehicle tax credits and hydrogen production credits after 2025.

The renewable supply chain’s reliance on Chinese inputs also implies vulnerabilities, given that the recent "foreign entity of concern" provisions included in the OBBB now limit access to components from adversary countries.

In addition, the executive order to boost the "clean coal industry" indicates a notable shift in US energy policy towards fossil fuels and critical minerals, likely redirecting funding and regulatory support from solar and wind towards coal, oil, gas and uranium production.

This comes in addition to other headwinds rattling the economic environment of the sector, such as high interest rates increasing financing costs, and surging prices for key materials like steel and copper, as well as components – notably as a consequence of the introduction of new import tariffs.

As a result, even though the upcoming phasing-out of tax credits under the OBBB should hasten the start-up of projects ‘under discussion’ or the completion of those already ongoing in the short term, and provide a temporary boom within the sector, US solar and wind energy developers must contend with a perfect storm of policy and business environment challenges.

Other clean energies face a brighter future

Fortunately, the entire clean energy sector is not set to face the same adverse climate. Non-solar and wind technologies such as storage, hydropower, nuclear and geothermal have been spared under the OBBB. Expanded tax credits remain in place, until at least 2033, when a progressive phase-down is foreseen for some industries. These technologies are now drawing significant investor interest.

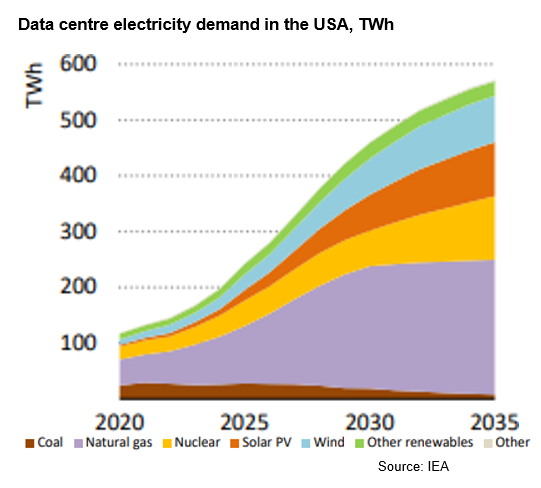

Another driver of innovation is the surging power demand from tech giants. After years of stagnant electricity consumption, data centres and artificial intelligence (AI) development are fuelling rapid growth in electricity demand. In the USA, demand is projected to increase by 2.2% and 2.4% in 2025 and 2026 respectively, according to the US Energy Information Administration (EIA), more than twice the average growth rate observed over the past decade. Meanwhile, the International Energy Agency (IEA) forecasts that the US economy, driven by AI use, is set to consume more electricity in 2030 for processing data than for manufacturing all energy-intensive goods combined, including aluminium, steel, cement and chemicals. Yet the specific energy needs of AI and data centres – demanding constant, high-capacity power – cannot be covered adequately by the variable output of solar and wind. Consequently, companies like Google are investing in advanced geothermal startups, and tech firms are also betting on next-gen small-modular nuclear reactors, signing deals with startups in the field.

In spite of this interest in alternative clean tech, natural gas – which is currently the largest source of electricity for data centres in the United States (see graph below) – is expected to continue to play a significant role in the additional power supply driven by data centre needs, followed by renewables, according to the IEA (April 2025). As a result, fossil fuels like natural gas and coal are still expected to power more than half of data centre capacity until 2030 in the USA.

Traditional power plants unlikely to replace stalled renewable projects

Given the current increase in power demand and the challenges facing solar and wind energy deployment, adequately bridging the gap created by delayed renewable projects with gas and nuclear power facilities may prove challenging. Indeed, with almost one fifth of gas power capacity in development already earmarked for data centres, new gas-fired projects face long waits (up to five to seven years) for specialised turbines. Nuclear plants are also slow to build, and advanced designs are only just reaching the prototype stage.

Renewables as a buffer against rising electricity prices

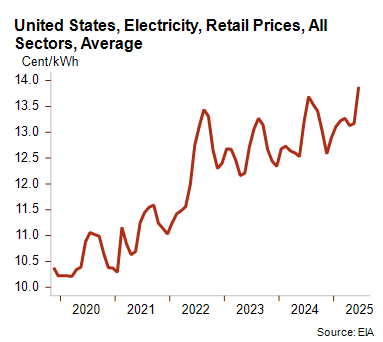

With electricity prices already rising (see graph below) due to surging demand from data centres and a recent increase in gas prices, growing energy demand and supply constraints should continue to push US electricity prices higher in the medium term. In this context, accelerating renewable energy deployment could curb prices, as it offers the lowest-cost option for new power generation and can be built faster than gas plants.

Analyst: Florence Thiéry – f.thiery@credendo.com