Mining sector: Iron ore and copper prices soared on the back of increased Chinese demand

Iron ore

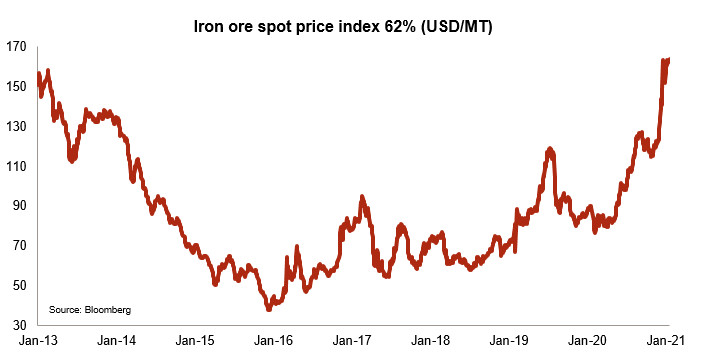

The key ingredient for steelmaking, iron ore was the asset in which to invest to ensure good returns during the Covid-19 pandemic. It barely suffered from the drop in demand at the start of 2020 and its price has literally exploded since December 2020, reaching USD 163/MT (+ 32% from 1 December 2020 to 12 January 2021), that is, 53% higher than the average for 2020, which was already exceptionally strong. The main reasons for this movement are, on the one hand, the iron ore production growing lower than expected and, on the other hand, the increase in Chinese demand.

Production was impacted, growing more slowly than expected (especially in Brazil), which suggests that demand could not be fully satisfied. The resumption of mining activities in the last quarter of 2020 could only partially compensate this. Global annual production increased by a small 4% in 2020 vis-à-vis 2019. Nevertheless, the increase in price should more than compensate the weaker supply of mining companies, likely to see their turnover increase for 2020.

As for demand, it followed an opposite path, simply due to the resumption of activities in China, supported by massive investments in infrastructure (steel-intensive), even though other major economies slowed down1. This shows the first risk underlying the iron ore market: its heavy dependence on Chinese demand (which represents 75% of global demand). Besides, China itself is heavily dependent on Australia for its iron ore supplies, as 60% of its imports come from there. In addition, the Chinese currency appreciated by 6% in 2020, which made iron ore more affordable for the Chinese importers and therefore supported its price.

As written above, the biggest risk for companies engaged in iron ore mining is a drop in demand from China, which will possibly happen again, leading to a lower iron ore price. In addition, the tense relationship between China and Australia could hamper China's supply of iron ore, affecting international prices and benefiting non-Australian producers. Another factor to watch is the development of China-US relations, which could also have an impact on the price. Furthermore, Chinese stocks are full, prompting buyers to reduce volumes to avoid buying at such high prices. Finally, the risk of depreciation of the renminbi against the US dollar would make iron ore more expensive, which is also a risk for producers (through price). Nonetheless, there are also upside risks for the iron ore price, like adverse weather or additional Covid-19-related restrictions that would affect the mining operations (as happened in Brazil in 2020). In the coming months, the price should remain elevated (in line with the average price in 2020, i.e. USD 105/MT) but we should expect it to slowly decrease over time.

Copper

Like that of iron ore, the price of copper has risen sharply since the start of the pandemic. The current price is 72% higher than the low reached in March. Just like for iron ore, China's rapid recovery is not for nothing in this rise and tensions between China and Australia and the depreciation of the US dollar had a role as well. But, unlike for iron ore, one must look beyond China. Indeed, the stimulus spending announced in the US and in Europe should further boost the demand for copper via two channels, namely household demand for all discretionary consumer goods which are copper-intensive (electric vehicles, ICT goods, etc.) and spending on renewable infrastructure projects.

Therefore, and unlike that of iron ore, the price of copper is expected to stay high over the long term, especially since inventories around the world are empty and mines’ output is limited. Some market analysts even expect a stronger rise in prices, so that the market is balanced.

The major risk for companies active in copper extraction therefore lies in a significant increase in supply (via scrap or new mines). However, this risk is mitigated given the time it takes to open new mines (environmental controls are increasingly restrictive and lengthy) and given that the necessary related infrastructure (for logistics) is often poor. Nonetheless, like for others metals, there are also upside risks for copper, such as adverse weather or additional Covid-19-related restrictions that would affect mining activities.

Given the rather limited current supply from copper miners and the increasing smelting capacities (above all in China), the treatment charge (TC, the fees paid by miners to smelters to process their ore into refined metal) is going down. Indeed, smelter operators have lower bargaining power. It should affect the margins of copper smelters.

Analyst: Matthieu Depreter – m.depreter@credendo.com

1 Imports of iron ore to China increased by 22% during the 11 first months of 2020 with respect to the same period in 2019.