Argentina: Despite economic and fiscal improvements, Macri has a hard time convincing voters

Event

Last year was a very challenging year for Argentina with a wide current account deficit (-5.4% of GDP) and fiscal deficit (-5.2% of GDP), a large depreciation of the Argentine peso (which lost about half of its value between 1 January 2018 and 1 January 2019), a jump in public debt (to a high level of 86.3% of GDP) and a skyrocketing inflation (roughly estimated at 50% at the end of 2018). This year is an important election year in the country as a new president will be elected. Hence, economic improvements will be crucial for the incumbent government to remain in power.

The government is enacting fiscal consolidation and the fiscal deficit is forecasted to improve to a deficit of -2.7% of GDP this year – still sizeable but much smaller than last year. As a consequence, public debt is expected to fall to roughly 76% of GDP in 2019, a high level still but clearly a significant improvement. The current account is ameliorating as well. First of all, thanks to exports picking up again after last year’s drought destroyed 30% of the country’s crops (agriculture products account for roughly half of Argentina’s export revenues). Secondly, thanks to imports contracting in response to the depreciating peso. In addition, foreign exchange reserves rose to covering 7.5 months of imports in March 2019 – a comfortable level – thanks to the improving current account and the disbursements of the record USD 56 billion IMF programme.

Despite these improvements, economic malaise continues in the country and recent opinion polls show that President Macri’s popularity is waning while former populist President Cristina Fernàndez de Kirchner’s popularity is on the rise. Although Kirchner will not run for president but for vice-president, her chosen president-elect (Alberto Fernández) might prove to be an important and likely populist opponent. In addition, last week, Argentina’s ruling coalition suffered a crushing defeat in the key regional elections of the province of Cordoba, the second-largest electoral district. A candidate of the populist Peronists party, to which Kirchner belongs, was elected in a landslide victory.

Impact

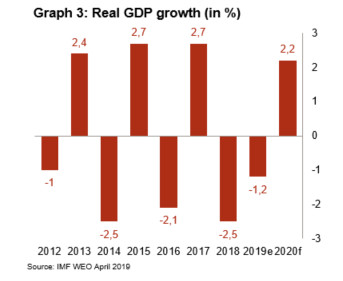

A narrowing fiscal deficit or current account deficit clearly doesn't win elections. The economic variables that influence electoral decisions are mainly peso volatility, inflation, poverty and consumption. In these four categories, the country is not performing well. Annualised inflation is projected to surge in 2019 and is estimated at a very high level of 56%. Furthermore, the Argentine peso depreciated by roughly 15% since the beginning of the year (last date: 20 May 2019). Also in the coming months, the currency will remain very volatile in the run-up to the presidential elections out of fear for the return of a populist president. Moreover, the economy remains in recession this year (real GDP growth of -1.2% is forecasted) after an already deep contraction of -2.5% last year. In fact, as Graph 3 shows, since the beginning of Macri’s term – in December 2015 – the economy has been in recession 3 out of 4 years. In turn, this has led to an increase of the unemployment rate and poverty levels (to roughly a third of the population).

Following the poor opinion polls, Macri returned to the imposition of price controls on basic consumer goods and allowed for salaries to increase in line with inflation. Additionally, with the blessing of the IMF, the Central Bank of Argentina is allowed to use its foreign exchange reserves and IMF resources to defend the Argentine peso. However, these policy measures are not uncontroversial as in the worst case it can lead to an inflation spiral and a depletion of foreign exchange reserves.

In the coming months, more opinion polls will appear but they might show different results depending on who decides to run (candidates have to register by 22 June) and with whom they’ll form an alliance. What is certain is that regardless of the election outcome, difficult times will lie ahead for the next president. Political polarisation is worsening and the next government is likely to face a narrower support base, rendering the ability to implement any economic policy more difficult. Furthermore, in the coming years heavy external debt service payments are in the cards while short-term debt and total external debt vis-à-vis current account receipts also are forecasted to stand at a high level. Lastly, access to the financial markets might prove to be difficult due to global risk aversion (e.g. recently triggered by the intensification of the trade war between the US and China).

For these reasons the medium-/long-term political and short-term political risk remain in the second-highest risk category of 6/7 while their outlook is negative.

Analyst: Jolyn Debuysscher– j.debuysscher@credendo.com