Nigeria: Will recent encouraging signs of economic progress last?

Highlights

- President Tinubu’s push to restore macroeconomic stability seems to be taking effect, despite the initially painful results.

- The naira is stabilising, and inflation is coming down after a period of sharp depreciation resulting from the exchange rate liberalisation.

- Fiscal reforms are targeting structural budgetary weaknesses like low public revenue collection, although significant loopholes remain.

- Nigeria remains in high-risk categories due to security risks, substantial debt servicing costs and oil dependency.

Pros

Cons

Head of State and of Government

Population

GDP per capita

Income group

Main export products

President Tinubu continues with his agenda of sweeping reforms

For many years, Nigeria’s costly parallel exchange market resulted in great inefficiencies and perceived corruption whilst structurally undermining investor confidence. This, along with persistently large capital flight, underperforming investment inflows and shocks in the oil market, kept liquidity under pressure. At the same time, there were concerns as to the sustainability of Nigeria’s public finances due to costly fuel subsidies and extremely limited fiscal revenues. When President Tinubu came to power in May 2023, he immediately embarked on an ambitious reform programme to revive the economy and attract investment. The impact of the unification of the parallel exchange rates and removal of fuel subsidies was deeply painful for most of the population. In fact, the liberalisation of the naira led to a spectacular 70% depreciation against the USD, due to which Nigeria’s GDP in USD-terms more than halved, from USD 476 billion in 2022 down to USD 188 billion in 2024. The same was observed for GDP per capita.

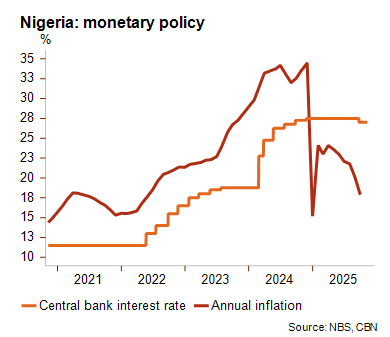

For more than two decades now, the poverty rate in Africa’s most populated country has been going up, driven by years of double-digit inflation. Following the naira-liberalisation, inflation took a leap up to 29% in 2023 (y-o-y) and peaked at 34% in November 2024. Together with the phasing-out of fuel subsidies, this led to a cost-of-living crisis and substantial social tensions. Following a statistical rebasing exercise, inflation plunged in December 2024 initiating a downward trajectory supported by the discontinuation of deficit financing by the Central Bank of Nigeria (CBN). In 2025, inflation dropped below 20% for the first time in almost 3 years, although the IMF does not expect the yearly increase in consumer prices to drop to 10% until 2029. In September 2025, the CBN announced the first policy rate cut in years. Economic growth exceeded 4% again in 2024 (3.9% projected for 2025) and even though it is still highly oil-driven, the contribution of non-oil sectors – like fintech and agriculture – is rising.

Is the tide turning on the deep deficiencies in public finances?

Despite headwinds and popular discontent, Tinubu’s government persevered with its reform strategy and since 2025 certain macroeconomic and fiscal metrics have started to improve. One of the striking deficiencies in Nigeria’s public finances is its low public revenues, the result of corruption and skimmed government funds. Oil theft and illegal bunkering are significant factors in these structural revenue shortfalls, and furthermore they cause great environmental damage and exacerbate insecurity in oil-producing regions. For years, Nigeria’s public revenues to GDP ratio barely reached 6%, among the lowest in the world, and well below the Sub-Saharan African average of 18% of GDP. Recent reforms to the tax system should help raise this ratio to about 10% of GDP this year, which is still a very low level for a large oil exporter, but is nevertheless a decisive leap forward.

Nigeria’s public interest burden is substantial, with a public debt stock of 39% of GDP in 2024 (30% in 2022). President Tinubu’s borrowing plan increased the proportion of external debt from a third of the total public debt stock in 2022 to almost two thirds in 2024, exposing Nigeria to exchange rate fluctuations and volatile oil prices. Another notable fiscal risk is the historic rise in accrued debts among Nigerian State-Owned Enterprises (SOEs), for which reliably documented figures are lacking. An extensive privatisation drive has been announced to address the contingent liability risk and improve the performance of these companies across all sectors.

Foreign exchange reserves are recovering

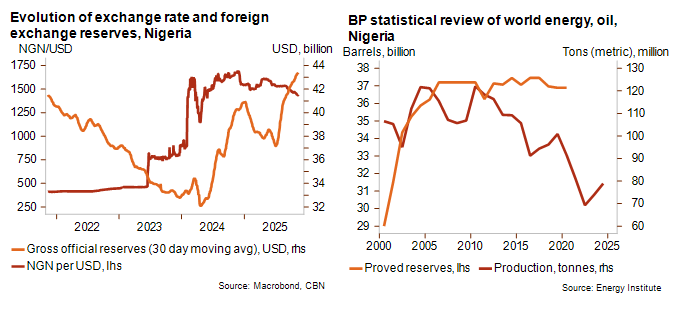

Between 2022 and 2024 Nigeria dealt with a persistent drop in foreign exchange reserves resulting from capital flight, a high debt servicing burden and falling oil production. Also, interventions made by the CBN to stabilise the naira added to the liquidity pressure. Following the shift to a managed float in mid-2023, pressure persisted amid uncertainty, but since early 2024, foreign exchange reserves have risen as CBN reduced interventions. Nigeria’s liquidity level has been further supported by large external loans, a temporary jump in oil and gas output and lower fuel imports (Dangote refinery), as well as with other import substitution measures. As a result, reserves have reached more than 43 billion USD again according to the CBN and would represent more than 6 months of import cover.

Significant risks that are holding back the African giant

Despite the enormous potential of Sub-Saharan Africa’s second largest economy and most populated country, structural weaknesses have kept it in high-risk categories. Security risks are substantial with jihadist activity and rampant banditry in the north-east, inter-communal violence between pastoralist (mostly Christian) and herder (mostly Muslim) communities over landownership in the central regions, and a low-intensity rebellion in the oil-producing Niger Delta. Another factor to consider is that US President Donald Trump has recently levelled accusations at the Nigerian government over what he has termed the slaughtering of Christians by Muslims, which is a grave and incorrect simplification of the complexity of conflicts in Nigeria. The subsequent threat of US military intervention caused as much surprise as it did concern and raises the risk for external conflict. In terms of socio-economic tensions, the high cost-of-living generates a sustained risk for protests and strikes across the country. In addition, the concentration of wealth and progress around the city of Lagos alienates most of the country, which could backfire at some point. This all results in a high political violence risk classification (category 6/7) which is factored into the general risk assessment for Nigeria.

Other major risks include Nigeria’s exposure to oil sector volatility; a deep and sustained drop in oil prices would immediately affect Nigeria’s financial position, and falling oil and gas production represents a significant long-term risk. Moreover, the debt servicing burden could undermine the recent progress made in terms of liquidity, and an abrupt rise in global interest rates could suddenly supercharge external debt pressures. It’s fair to say that Nigeria still has significant risks as a market, but at the same time it has enormous potential, and recent developments indicate encouraging progress (from the current MLT political risk rating in 6/7).

Analyst: Louise Van Cauwenbergh – l.vancauwenbergh@credendo.com