Türkiye: Resilience tested by conflict in the Middle East and weak liquidity

Highlights

- A resilient economy, well-diversified current account receipts, well-developed banking sector and dynamic corporate sector.

- Strong solvency and solid public finances.

- Main weaknesses include a reliance on short capital flows and energy imports.

- A more orthodox monetary policy has been in place since mid-2023, but foreign exchange reserves remain volatile, exchange rates are still under pressure and inflation is at double-digit levels.

- The country risk outlook depends on the duration and severity of the conflict in the Middle East.

Pros

Cons

Head of State and government

Population

GDP per capita

Income group

Main export products

A well-diversified and resilient economy

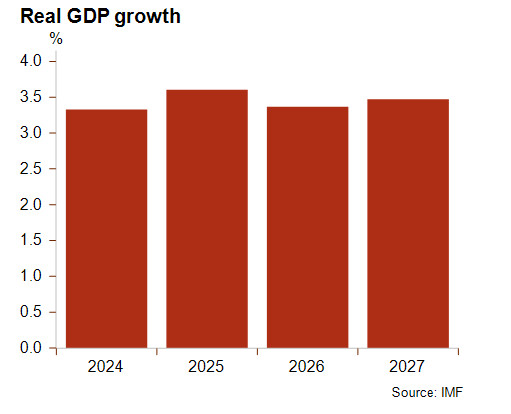

Türkiye’s economy is characterised by well-diversified current account receipts, a well-developed banking sector, a dynamic corporate sector and resilient economic growth. Real GDP grew by 3.6% in 2025, although it is expected to slow down in 2026 amid the large surge in energy prices – provoked by the conflict in the Middle East – even though the share of renewables in electricity production has increased in recent years, reducing its dependency on hydrocarbons for electricity generation. Moreover, the expected economic deceleration in the Middle East will have a negative impact on the country, as goods exports to the Middle East accounted for almost 20% of the total in 2024, making it Türkiye’s second trading partner after the EU (which accounted for almost 40% of goods exports in 2024, implying that competition in the high-emission intensity sector such as steel, cement and aluminium could be harmed by the EU Carbon Border Adjustment Mechanism (CBAM)). The US accounts for only 6% of goods exports, and therefore the volatile and uncertain US protectionist policies, not to mention US tariffs, have a limited direct impact on the Turkish economy.

Despite a negative net foreign asset position and asset-quality deterioration, as shown by an increase in the non-performing loan ratio to 2.5% in December 2025 from 1.8% a year earlier, the banking sector is well developed and supports the dynamic corporate sector. Domestic corporate debt surged over the last decade, hitting a high of 75.5% of GDP in Q3 2020, but has dropped since then, falling to 39.1% of GDP by Q2 2025, however it remains exposed to FX risk.

Appointment of a team with a more orthodox macroeconomic policy in mid-2023

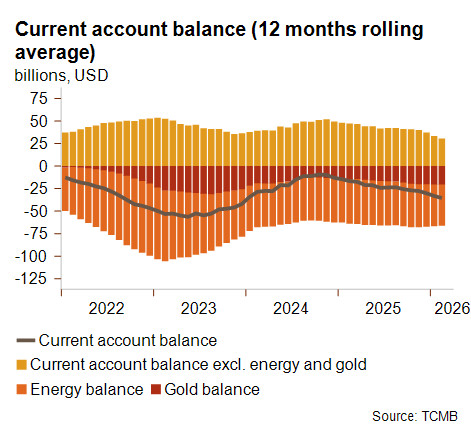

The current account deficit narrowed in 2024–25 compared to its 2022–23 level; this improvement is related to lower net gold imports (which is largely shaped by domestic confidence as purchasing gold serves as a way to safeguard savings during periods of high inflation) and lower net energy imports. This can also be partly attributed to a turnaround in macroeconomic policies. Following his re-election in May 2023, President Erdoğan appointed a team with a more orthodox economic approach led by Finance Minister Mehmet Şimşek. As shown by the graphs, the central bank increased its benchmark interest rates, allowed the Turkish lira to depreciate and withdrew some unorthodox financial instruments in mid-2023. These policy changes resulted in a sharp depreciation of the Turkish lira, which has heightened inflationary pressures. Nevertheless, these measures have contributed to a gradual reduction in macroeconomic imbalances, including the narrowing of the current account deficit and a sustained decline in inflation, although this remains elevated (see graph). Looking ahead, the sharp increase in energy and food prices, currently driven by the conflict in the Middle East, is likely to put renewed pressure on inflation and widen the current account deficit, along with an expected decrease in tourism that represented almost 15% of current account receipts in 2024.

The appointment of a more conventional economic team in mid-2023 significantly bolstered foreign investor confidence, enhancing Türkiye’s access to global financial markets. This is particularly significant given the country’s continued reliance on portfolio flows to finance its (now lower, but still rising) current account deficit, despite a notable decrease in dependency. The stock of portfolio investment accounted for around 18% of foreign liabilities in 2024, a significant decrease from about 77% in 2017. These figures, together with the marked improvement in the net international position (from about -50% of nominal GDP in 2017 to about 25% in 2024), further underscore the positive developments in Türkiye’s macroeconomic situation.

Volatile and limited foreign exchange reserves, but strong solvency

However, any erosion of foreign investor confidence, as witnessed in March 2025 following the arrest of Istanbul Mayor Ekrem İmamoğlu, can result in considerable capital outflows and a sharp reduction in gross foreign exchange reserves (excluding gold, which constitutes an important share of official foreign exchange reserves). Although reserves have partially recovered since then, they continue to exhibit volatility. In March 2026, they dropped sharply again upon the onset of the conflict in the Middle East, highlighting that the country remains vulnerable to external shocks as well as the tendency of the authorities to intervene to stem sharp exchange rate depreciation. In any case, the exchange rate continues to depreciate.

On the positive side, Türkiye’s solvency position remains strong, supported by moderate external debt and a low debt service. However, its Achilles’ heel is its poor, albeit improving, liquidity position. Meanwhile, short-term external debt remains high and the level of gross foreign exchange reserves, excluding gold, is limited – covering less than three months of imports – and remains highly volatile (see graph).

Sound public finances

Since Erdoğan’s re-election, fiscal policy in Türkiye has become less expansionary. Nonetheless, the primary balance is still slightly negative, while the overall fiscal deficit remains above 3% of GDP due to rising – but still moderate – interest payments. Overall, public finances are solid, with public debt staying close to 25% of GDP and 100% of public revenue, but the earthquake in 2023 was a reminder that Türkiye remains vulnerable to natural disasters. Finally, a large influx of refugees amid the war in Iran could also put pressure on public finances, as well as on rents (and thus inflation), while a further risk related to the conflict in the Middle East is that Türkiye – a NATO member and a mediator between Iran and the US alongside Pakistan and Egypt – could be targeted by Iranian missiles.

Country risk classifications

The policy turnaround implemented following President Erdoğan’s re-election in 2023 contributed to a reduction in the structural current account deficit, a notable decline in inflation and an improvement in foreign investor sentiment. As a result, liquidity conditions improved, despite continued volatility in gross foreign exchange reserves and pressure on the exchange rate. Given Türkiye’s low levels of external and public debt, its large, diversified and resilient economy and significant geopolitical importance, Credendo has upgraded its ST and MLT political risk to category 4/7 (from category 5/7), despite the deterioration in quality of the institutional framework over the past decade, as shown by the decline of the World Bank governance indicators (government effectiveness, regulatory quality, rule of law and control of corruption). The business environment risk was then downgraded to category G/G after the outbreak of the latest conflict in the Middle East, because despite a resilient economy, the potential repercussions include an expected rise in inflation, a larger current account deficit caused by increased energy prices, reduced demand from the Middle East, and an expected decline in tourism. In addition, this classification also reflects the above-mentioned deterioration in the quality of the institutional framework, persistently high inflation (which weighs on nominal interest rates) and sustained pressure on the exchange rate.

Analyst: Pascaline della Faille - P.dellaFaille@credendo.com