Uganda: Middle East conflict exposes short‑term risks despite Uganda’s imminent oil start‑up

Event

Uganda’s long‑anticipated shift from fuel importer to crude oil exporter is expected later this year, with technical start‑ups planned around July and first crude exports anticipated by October. Production is centred on the Kingfisher Project (CNOOC‑operated) and Tilenga Project (TotalEnergies‑operated) in the Lake Albert basin. Together, these projects are expected to lift output towards a plateau of around 230,000 barrels per day once fully operational.

Impact

The ongoing conflict in the Middle East, the resulting damage to energy infrastructure and the effective closure of the Strait of Hormuz have caused a sharp rise in energy prices and heightened concerns regarding potential energy shortages. However, the increase in oil prices could benefit Uganda, as the country is expected to commence oil production in the near future. While by April 2026 the East African Crude Oil pipeline (EACOP), which will transport crude oil to the Tanzanian port of Tanga, is approximately 82% complete, the construction of the Hoima refinery has yet to start. This implies that Uganda remains at risk of refined fuel shortages since it continues to rely on imported refined fuel, primarily supplied via the Kenya Pipeline Company. As a landlocked economy, Uganda is particularly exposed to inflationary pass‑through given that higher global fuel prices feed directly into transport costs and, in turn, into domestic prices across the economy.

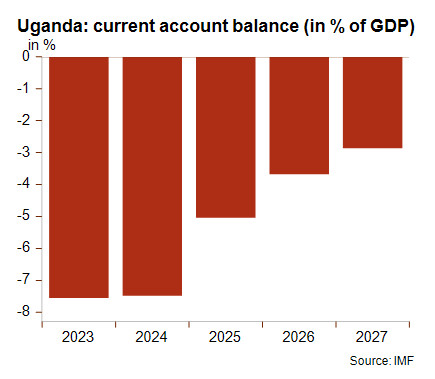

The Middle East conflict has also provoked interruptions in fertiliser supply (and supply of other materials), reduced remittances from the Gulf region and worsened financial conditions. As a food exporter – with coffee as an important source of current account receipts – Uganda is exposed to higher fertiliser costs and possible shortages given its reliance on Middle Eastern suppliers. Remittances – the country’s second largest source of current account receipts – are another contagion channel, as roughly one third of inflows originate from the Middle East, where more than 200,000 Ugandans are estimated to be working. Looking ahead, even though these sources of current account receipts might be under pressure, the onset of oil production would lead to a narrowing of the current account deficit. Indeed, oil infrastructure development has contributed to sizeable and persistent current account deficits over recent years (see graph below). However, this deficit has predominantly been financed through the FDI inflows linked to these projects, thereby largely mitigating external financing risks.

Nonetheless, Uganda continues to face several structural constraints. The high share of food in household expenditure leaves Ugandans particularly exposed to cost of living pressures. Institutional weaknesses are illustrated by high corruption perception and accountability gaps, while the political climate remains strained following the January 2026 elections. Moreover, Uganda remains reliant on external budget support in a context of tightening global aid while high public interest payments absorb a growing share of government revenues, limiting fiscal flexibility and the capacity to absorb shocks.

For now, Uganda’s MLT political risk classification in category of 6/7 and ST political risk classification in category of 4/7 remain appropriate. Nevertheless, if the conflict in the Middle East persists, resulting rising inflation and potential fuel shortages could exert downward pressure on the business environment risk rating, currently assessed at E/G.

Analyst: Jonathan Schotte – j.schotte@credendo.com