Democratic Republic of the Congo: Upgrade from 7 to 6 for medium- to long-term political risk

The DRC is increasingly considered an indispensable part of global supply chains

The DRC holds by far the world’s largest share of cobalt, which accounts for about 70% of global production, while it also contains some of the world’s largest reserves of copper, coltan, lithium, and other critical minerals foundational to clean energy transition, advanced technologies and modern industries. Over the past 30 years, most Western investors have left the DRC, leading to a situation where about 90% of major stakes are estimated to be held by Chinese entities today. Over recent years, a boost in American, European and Gulf States’ interest in various mines and consortiums across the country has been observed. America’s recent commitment is an immediate opportunity to diversify beyond Chinese investments and negotiate better deals, involving actual added value. Europe’s expanding efforts to re‑engage in mining across Africa translate into the Global Gateway Initiative. The Gulf, on the other hand, is grappling with the repercussions of the war in the Middle East, which negatively impact its investment ambitions in Africa.

Economic growth and liquidity could be lifted by global race for strategic minerals

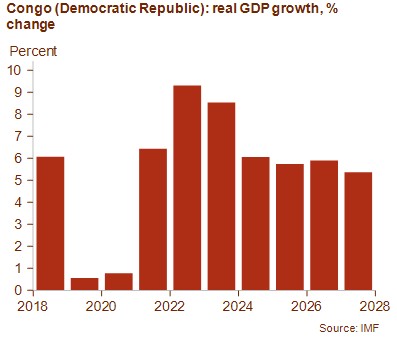

Decades of conflict and instability have left the DRC with very weak governance and institutional indicators, a fragile banking system and poor infrastructure, while corruption perception remains among the highest globally. This weighs on economic and human development, together with a structurally low saving rate – the DRC having one of the world’s poorest populations. Still, economic growth is projected to reach almost 6% this year and 5.4% in the coming years. This is largely due to roaring demand for critical minerals, bringing the country to the forefront of a global commodity boom driven by large powers trying to secure their long-term access to these strategic assets.

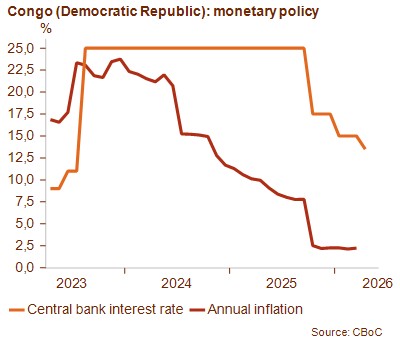

On the monetary front, progress has also been made. After years of high inflation, inflation has come down since 2024 to reach 2.3% in 2025. As a result, the monetary policy has been loosened three times since last year – prompting a policy rate cut from 25% to 13.5% – while the Congolese franc recovered from a depreciation at the end of 2025. However, the DRC is highly exposed to soaring global energy prices caused by the war in the Middle East, as fuel imports represent about 23% of total goods imports. Therefore, current account and fiscal deficits are likely to widen, inflation is expected to rise to 7% again by the end of the year through higher transportation and food prices, while a weaker local currency will raise the foreign currency-denominated debt burden. Yet, given the favourable starting point, external debt indicators are expected to absorb the shock, at least in the near term.

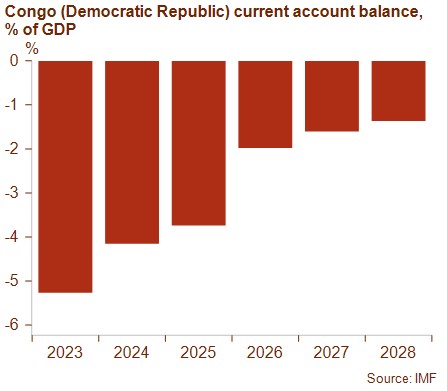

The current account should remain in a small manageable deficit, although pressure on liquidity is still high. Foreign exchange reserves are tight at around two months of import cover, despite its doubling since 2022 thanks to rising mining revenues and renewed IMF support. The wide use of the USD in domestic transactions (dollarisation) limits the central bank’s ability to manage liquidity and build reserves. Exports of metals and minerals account for almost 96% of the DRC’s total export revenues, creating high vulnerability of external and fiscal balances to price and output swings in the mining sector. The DRC’s substantial reliance on aid funding (ODA accounted for 12% of current account expenditures in 2023) also exposes it to the global shortfalls in donor financing, raising social and instability risks amid the country’s enormous humanitarian needs. Since last year, the DRC has entered a new Extended Credit Facility programme (January 2025–March 2028) with the IMF, helping cover its large external financing needs. At the same time, the DRC’s vast mineral endowments create large potential for capital investment inflows, raising prospects of covering the current account deficit, and hence lowering the external financing gap.

Low external debt burden supports acceptable financial position and public finances

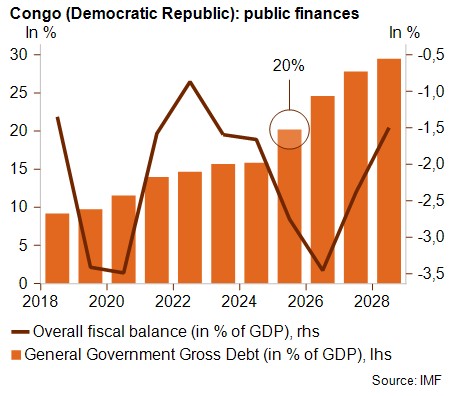

After being shielded from international financing for decades and thanks to HIPC debt relief completion in 2010, the DRC has very low external debt ratios (around 15% of GDP in 2025). The IMF currently projects this debt-to-GDP ratio to remain relatively stable by 2030, while debt services continue to absorb a negligibly small part of current account revenues. Given this highly favourable starting point, external debt and debt servicing indicators should remain within sustainable territories, at least in the coming years, which underpins the decision to upgrade the DRC’s MLT political risk classification from the highest category 7 to category 6. Public finance figures are also favourable with confined fiscal deficits and a public debt stock at 20% of GDP in 2025, projected to grow to 33% of GDP by 2030. Still, institutional weaknesses affect the budget’s reliability, while rising security spending are crowding out other essential expenditures and overreliance on the mining sector for revenues sustain a risk for non-payment in government transactions.

High risk for political upheaval and decades-long conflicts affect wide swaths of the DRC

For decades, the DRC has been the scene of multiple interlinked security crises, recently dominated by the conflict in the eastern provinces, which deteriorated since Rwanda-backed M23/AFC (March 23 Movement/Alliance Fleuve Congo) rebels took large parts of North and South Kivu in early 2025. Ever since, rebels have installed a violent occupying force in the region. Qatari, Angolan and US-brokered peace deals had little impact on the ground as local fighting quickly resumed, emphasizing the limited influence of state-level accords on non-state armed groups. Over 100armed groups operate across the DRC’s mineral‑rich eastern regions of North and South Kivu and Ituri, while other regions, such as Mai-Ndombe, Tanganyika, Haut-Uele, Maniema and Haut-Lomami, are affected by ethnic grievances or land-related conflicts that lead to local clashes and drive displacement. Due to this very unstable political and security context, a restrictive approach towards regions affected by armed conflict or frequent occurrence of violent attacks is upheld, excluding all cover in these regions.

The loss of eastern capital cities Goma (North Kivu) and Bukavu (South Kivu) has undermined confidence in President Tshisekedi’s ability to secure the country and enforced the opposition. In Kinshasa, this has led to fierce opposition crackdowns, constitutional amendments and a sustained risk of President Tshisekedi getting ousted, while the Armed Forces of the Democratic Republic of the Congo (FARDC) remain highly prone to mutinies. Ex-president Kabila’s ties to certain rebel groups are another element increasing the risk for political turmoil. Nevertheless, it remains unlikely for rebels from the east to march on Kinshasa, not in the least because of enormous logistic obstacles.

Although it is expected that cooperation with international partners – especially the US – will help cement Tshisekedi’s position, the risk for political upheaval remains high. The December 2025 ‘Washington Accords’ pair American support with long‑term access to the DRC’s critical minerals, expanding resource extraction despite persistent violence and lacking grasp on the core drivers of conflict in the region. With the involvement of troops from neighbouring Burundi, Uganda and South Africa, the conflict also has regional implications, risking reviving the wider regional war that engulfed Africa two decades ago.

Analyst: Louise Van Cauwenbergh – l.vancauwenbergh@credendo.com