Tajikistan: MLT political risk upgrade from category 7/7 to 6/7

Improved fundamentals allow a MLT political risk upgrade

On the back of gradually improved macroeconomic fundamentals over the past years and an overall positive economic outlook, Tajikistan appears to be able to capitalise on this progress for the years to come. Therefore, Credendo has upgraded the country’s MLT political risk rating from category 7/7 to 6/7.

Despite multiple shocks (Covid-19 and the war in Ukraine), the Tajik economy has shown resilience over the 2020–2024 period, posting a strong average 7.7% GDP growth rate and relatively contained inflation. Though GDP growth forecasts are less impressive, with a gradual deceleration expected towards 4.5% in the MLT, the economy will remain supported by rather good macroeconomic fundamentals. Public finances are quite comfortable with public debt expected to stay under 30% of GDP and a moderate fiscal deficit of around 2.5% of GDP. The same positive picture applies to the balance of payments, as the current account deficit is forecasted to be contained at around 5% of current account receipts in the coming years, following a surplus in 2020–2024.

Liquidity has been much strengthened

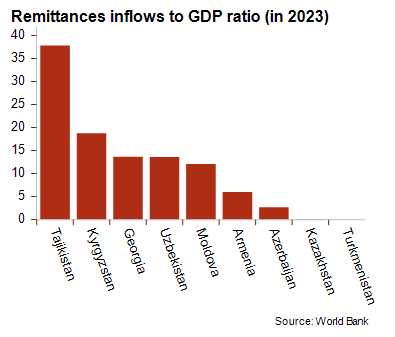

Compared to the pre-Covid years when liquidity was constantly under pressure, sharply strengthened foreign exchange reserves greatly improved the import cover, which reached 5 months last September. This has a lot to do with the strong support from Tajik workers’ remittances from Russia and labour income. These almost account for 85% of total current account receipts, which is at the same time a high vulnerability. Until now, the ongoing crackdown against Central Asian migrants in Russia, following the terrorist attack of March 2024 in Moscow, does not seem enough to deter Tajik workers away from Russia given its financial attractiveness. Moreover, Russia also badly needs these workers to cope with labour shortages.

Other sources of current account receipts arise from mining (gold, aluminium) and hydroelectricity. The completion of the huge and long-standing Rogun hydropower project, the world’s tallest dam, would further boost export revenues from hydroelectricity but the dam is not expected to reach full capacity before 2033.

Tajikistan’s improved macroeconomic fundamentals are expected to persist, reflecting the authorities’ goals of economic and financial stability as proved by the good implementation of the current IMF Policy Coordination Instrument. Though the external environment and global economic outlook are deteriorating amid the US-driven global trade war, Tajikistan is a minor trade partner of the US, which should limit the negative impact.

A high external debt service and climate change vulnerability weigh on the risk outlook

The financial situation remains the most important MLT risk for Tajikistan despite moderate external debt. Indeed, the country has a large debt service for the coming years, which is a source of risk given the country's structural weaknesses. This can be explained by the repayment of the 2017 Eurobond, due in 2025–2027, and the fact that a higher share of the external debt is non-concessional since the country graduated to lower-middle income in 2020. The high vulnerability to climate change is another major downside risk. Indeed, the country is expected to warm up relatively quickly over the next decades, increasing its exposure to powerful droughts and floods, and erratic precipitation. The dominance of water-dependent agriculture and hydropower sectors leaves the economy vulnerable to climate shocks while adaptation capacity is weak.

Like Central Asian peers, the country is politically stable but under firm control of President Rahmon. Institutions are very weak – having one of the world’s highest levels of perceived corruption – and hence represent a major MLT risk. On the security side, relations have improved with neighbour Kyrgyzstan, culminating in a historic border agreement that ended decades of conflict in March 2025. However, Tajikistan remains exposed to a deterioration of the security situation in Afghanistan because of the porous borders.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com