Indonesia: Economic buffers will mitigate the Middle East conflict shock

Highlights

- Indonesia’s historic economic resilience is likely to continue in the coming years on the back of solid macroeconomic buffers.

- However, a record-low rupiah reflects the widening current account deficit, eroded investor confidence vis-à-vis fiscal credibility and rising State interventionism in the economy, fuelling capital outflows and weighing on liquidity levels.

- In the long term, Indonesia is well placed to benefit from shifting supply chains through trade deals and potentially strong commodity exports related to critical minerals and clean technologies.

- The stable outlook for the ST and MLT political risk will face climate risks and increased social discontent.

Pros

Cons

Head of State and Government

Population

GNP per capita

Income group

Main export products

Economic resilience challenged by external shocks

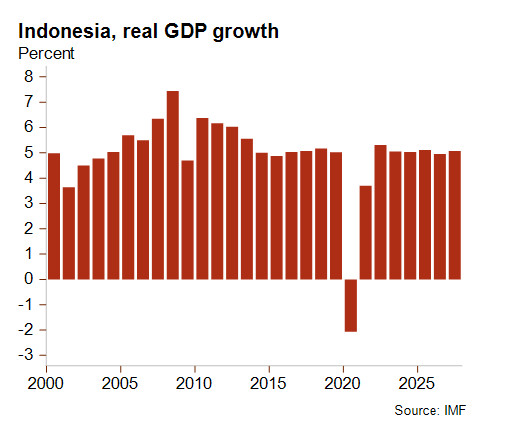

Historically, the Indonesian economy has high levels of resilience. Unlike most countries in the region, it relies more on private consumption in relative terms and is comparatively less vulnerable to external shocks. Therefore, real GDP was able to grow by an average of 5% over the past decade (excluding the Covid-19 shock in 2020–21) and is forecast to remain stable at this level in the coming years. This is a good growth rate for a country defined as having ‘upper-middle income’ since 2023, yet far from the overly optimistic 8% promised by President Prabowo when he came to power in 2024, with the vision of bringing Indonesia into the high-income bracket by 2045.

Nonetheless, the Indonesian economy is suffering from the global energy crisis fuelled by the current conflict in the Middle East. Although Indonesia is a net fuel exporter, it is also a net oil importer, with 20% coming from the Gulf region – which also supplies more than 40% of its gas. In response to this shock, the government froze fuel prices and rationed energy use. However, reducing fuel subsidies was not considered in order to prevent inflationary pressures from hitting key private consumption and avoid the risk of reigniting last year’s mass Gen-Z protests, primarily against the cost of living and rising youth unemployment. As a result, inflation fell to 2.4% in April but at high fiscal costs. Meanwhile, higher imported input costs (for goods such as fertilisers) could fuel inflation and constrain the Central Bank’s ability to lower its policy rate in support of the economy. President Prabowo’s recent visits to Japan, South Korea and Russia were an attempt to seek out investments and support for speeding up the energy transition, in order to improve energy security and better withstand future external shocks. Likewise, the exploitation of a recently discovered major offshore gas field from 2028 could help to ease energy supply concerns and alleviate pressure on energy imports.

Stable political risk level hit by the Middle East conflict shock and investor doubts on government policies

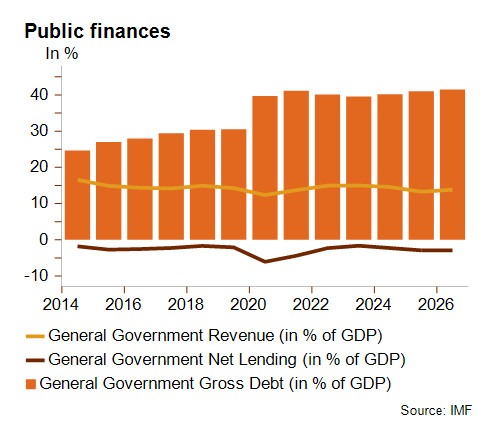

Until now, Prabowo’s presidency has coincided with weakening macroeconomic fundamentals and investor perception. In addition, the fiscal deficit is close to the legal ceiling of 3% of GDP, partly as a result of the bold free school meal plan and various welfare projects but also due to transfers to the new Danantara sovereign wealth fund and growing defence spending. Public debt (41% of GDP in 2025; 10 percentage points higher than pre-Covid levels) and interest payments are slowly on the rise, but there are concerns regarding the continuing low level of government revenues that fell to a five-year low in 2025 (13.3% of GDP), keeping the public debt-to-revenues ratio above 300%. Though public spending cuts and some extra tax measures aim to offset swollen fuel subsidies this year, protracted high oil prices will be more difficult to manage for the government. Therefore, investor pressures surrounding the potential loss of Indonesia’s investment grade rating could continue amid shaken fiscal credibility.

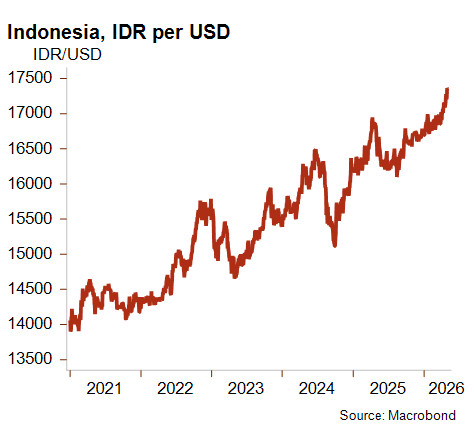

The current account deficit is also expected to increase substantially this year – though still remaining at a low level overall – from 0.1% to 1.1% of GDP due to fallout from the war in the Middle East and costlier imports. These domestic and external factors have contributed to frequent depreciation pressures on the Indonesian rupiah (around -15% against the US dollar since Prabowo’s election). The currency’s slide to a historic low is also related to capital outflows, reflecting investor doubts concerning a perceived reduction in the independence of the Central Bank and the justice system with the military being granted a growing role in civil institutions. Although a strengthening of State interventionism in the commodity sector (starting with palm oil, nickel and coal) was announced in mid-May with the aim of increasing government revenues, this has done nothing to improve investor confidence.

Nevertheless, these deteriorations come off the back of a solid economic position and historically cautious economic management. In addition, Indonesia maintains a low financial risk with a sustainable external debt (under 30% of GDP) and adequate liquidity levels. These factors help to explain the stable outlook for the ST and MLT political risk rating, namely 2/7 and 3/7 respectively. At the same time, the drop in foreign exchange reserves since 2025 – partly explained by capital outflows and the Central Bank’s interventions to stabilise the rupiah – deserves attention. Import cover fell to slightly more than four months in March, the lowest level seen since mid-2024, and could drop further in the short term on the back of more expensive imports.

Trade deals, supply chain diversification and a strong export outlook

Only a few days before the start of the conflict in the Middle East, Indonesia reached an unpopular trade deal with the USA. On 19 February, Jakarta agreed to significant concessions (no import tariffs on nearly all US exports of goods, the removal of many non-tariff barriers including local content requirements, commitments of large purchases of US goods such as aircraft, etc.) in exchange for a tariff cut from 32% to 19% on Indonesian exports of goods and, more significantly, for zero tariffs on key commodities such as palm oil. However, the following day the US Supreme Court ruled that US reciprocal tariffs were illegal. Trump’s subsequent decision to adopt a global 10% tariff, which was raised to 15% the following day and is also being contested legally, creates uncertainty regarding the future implementation of the bilateral deal in its current form – even though Jakarta will most likely seek to avoid any tensions with Washington. Irrespective of the US import rate, trade dependence on the USA (10% of goods exports) remains moderate and far less pronounced than other Asian countries. Indonesia is much more reliant on its first trade partner, China (22% of goods exports and 32% of goods imports) and Jakarta intends to give priority to more reliable trade deals, starting with the Regional Comprehensive Economic Partnership: the world’s largest free trade agreement. Also of note is Indonesia’s conclusion of new bilateral trade deals over the past year with the European Union, the Eurasian Economic Union and Canada, highlighting its policy of supply chain diversification and echoing its historically non-aligned foreign policy and non-involvement in superpower competition.

The Indonesian government aims to expand exports while strengthening economic resilience and security, and the country is well placed to benefit from the global energy transition and rising demand for clean technologies. Indeed, Indonesia is rich in commodities, including critical minerals dominated by copper and nickel, and is the world’s number one producer for the latter. Prabowo wants Indonesia to be a major player in global critical mineral supply chains, promoting self-sufficiency and expanding on his predecessor’s policy of resource nationalism. This has been demonstrated through an export ban on unprocessed nickel and rare earths. The growing demand for EV batteries, driven by Chinese investments, is leading to booming exports of processed nickel, accounting for 3.5% of Indonesia’s goods exports in 2025. Nickel (affected in the short term by high sulphur prices), palm oil (boosted as a biofuel amid Gulf fuel shortages), steel and manufacturing (including an emerging solar panel industry) all contributed to a 6.5% expansion of goods exports last year. With optimistic forecasts for batteries and EVs, they are likely to remain key export growth drivers for the years to come.

Overall, Indonesia’s diversified economy and good macroeconomic fundamentals are buffers against future external shocks in a fast-evolving geopolitical and trade environment. If managed well, Indonesia could reap the fruits of shifting supply chains in the region. However, in addition to the risks associated with a more unpredictable and interventionist president, Indonesia’s stable economic outlook currently faces a broad range of downside risks, from a high level of vulnerability to climate risks and intense Chinese competition for local companies, to a constrained fiscal policy, a decreasing middle class and renewed socioeconomic discontent.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com