LATAM: 100 days of Trump changed the geopolitical and economic game for Latin America

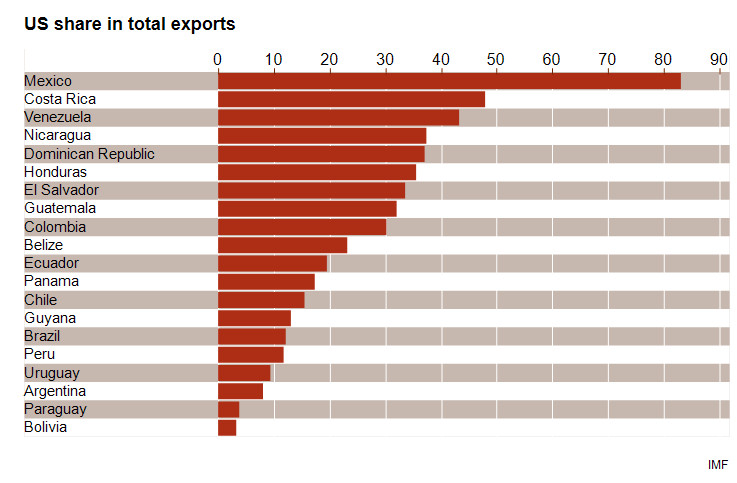

The escalation in trade war during Trump’s first 100 days hurt Central America the hardest

During the 100 days that followed Donald Trump’s inauguration in January, a new and more intense phase in the global trade conflict has emerged. Previously centred on the US-China rivalry, the trade war expanded into a global trade war. On 9 April, President Trump imposed a 10% blanket tariff on all imports, significantly impacting Central America due to its heavy reliance on exports to the United States (see graph below).

As the region’s largest exporter to the USA, Mexico has been particularly affected, especially with the 25% tariff implemented on 4 March for goods that do not comply with the United States-Mexico-Canada Agreement. As a result, Mexico is experiencing a significant economic strain: the Mexican peso depreciated by 15% year-on-year vis-à-vis the USD, a shallow recession is forecast for this year and current account revenues are declining.

In contrast, South America has been less affected by US tariffs. This is partly due to the smaller proportion of its goods exports being destined for the USA, and because commodities, such as energy and copper (which are major sources of current account revenues), are currently exempt from these tariffs.

Latin America escapes the threat of reciprocal tariffs, but is not out of the woods

Latin America escapes the threat of reciprocal tariffs (with notable exceptions for Venezuela, Guyana and Nicaragua, although these have been paused for 90 days), given most countries run bilateral trade deficits with the USA. However, Latin America is not out of the woods. First of all, the region remains in the USA’s sight as it is perceived by the USA as its sphere of influence. Trump has demonstrated his use of tariffs as a tool to coerce the region into accomplishing several policy objectives, including political (Venezuela, Cuba, Nicaragua), security (Mexico), immigration (Colombia, Guatemala, Nicaragua, etc.) and US-China tensions (Panama Canal, Chancay port in Peru). This situation leaves countries, especially in Central America, vulnerable to further tariffs. Secondly, the rising risk of a recession in the USA could affect the region, as it would result into lower remittances (especially to Central America) and decreasing oil prices (which are already under pressure with the recent drop in oil prices following OPEC+ decision to increase production).

Chinese dumping risks and US tariffs may deepen Latin America’s commodity dependence

Since Trump took office, the cooperation between China and Latin America has accelerated. This increase in trade with China is likely to deepen Latin America’s dependency on commodities for current account revenues, as China primarily seeks raw materials rather than finished products. Additionally, US tariffs are mainly targeting value-added finished goods, while the USA is a key market for these goods. Moreover, the region is also particularly exposed to the dumping of Chinese products originally destined for the USA. Several countries might receive low-cost Chinese imports, particularly in sectors such as steel, automotive (parts) and electronics. This influx may undermine domestic producers and create new trade barriers, especially in more industrialised economies like Brazil, Mexico and Argentina.

Analyst: Jolyn Debuysscher – J.Debuysscher@credendo.com