Kenya: Debt-driven vulnerabilities persist despite short-term liquidity relief

Event

In February 2024, the Kenyan government unexpectedly issued a new USD 1.5 billion Eurobond with a seven-year maturity and used the proceeds to pay back the Eurobond maturing in June of that year. In February 2025, Kenya repeated this feat with another USD 1.5 billion Eurobond, this time with an 11-year tenor. The proceeds were used to refinance a 2019 Eurobond maturing between May 2025 and May 2027. This means that Kenya’s next maturing Eurobond comes due in February 2028.

Impact

The 2024 and 2025 bonds were costly, with yields of 10.375% and 9.95% respectively; significantly higher than the yields paid by the Kenyan government in the past. The USD 3 billion raised has helped boost foreign exchange reserves to their highest level ever, with reserves covering close to five months of imports for 2025.

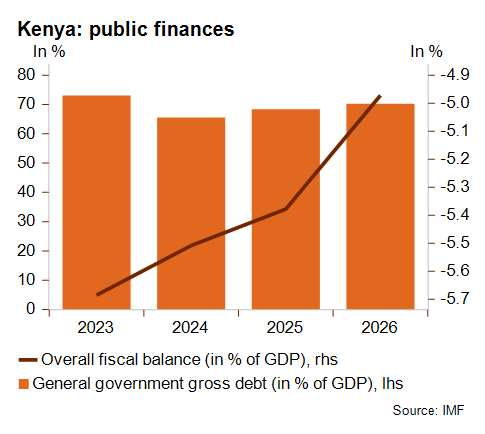

While these issuances have eased short-term refinancing pressures, Kenya’s public and external debt sustainability remains a reason for concern. Public debt to GDP is high, at 70% of GDP (see graph below) and almost 380% of public revenue in 2024. The country also has a sizeable (but decreasing) fiscal deficit. The ratio of public interest payments to revenues is particularly noteworthy and is projected to average 29.1% over 2024-2028.

To improve the public finances, the Ruto government tried to implement the “2024 Finance Bill”, which aimed at raising taxes. However, persistent and widespread protests forced the government to withdraw the bill. As a result, the authorities have missed structural benchmarks and fiscal targets set in the IMF programme. In March 2025, Kenya and the IMF mutually agreed to end the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) programmes, just one month before their scheduled end. This implied that Kenya did not receive the final disbursement of the programme (about USD 490 million), and USD 400 million under a separate IMF Resilience and Sustainability Facility. Kenya has requested a new IMF programme, but this has not yet been finalised.

The withdrawal of the Finance Bill did not only impact Kenya’s fiscal trajectory but also underscored the broader challenges facing the country’s domestic political landscape. Kenya’s political situation has been marked by recurring unrest over the past few years, reflecting deep-rooted tensions and public dissatisfaction. Large-scale public protests have taken place every year since 2022. Although there have been different triggers, such as the opposition rejecting President Ruto’s election victory or the 2024 Finance Bill, frustration over the rising cost of living is a recurring theme. The most recent protests started in early June, triggered by the death of blogger Alber Ojwang in police custody, and also expressed frustration at economic hardship and alleged government corruption.

Alongside its public debt, Kenya’s external debt has also grown sharply over the last decade to 70% of GDP in 2023 and more than four times the current account receipts. The export base of the East African nation has not expanded at a comparable rate.

In this context, the MLT political risk classification in category 7/7 and the ST political risk classification in category 5/7 remain appropriate for now.

Analyst: Jonathan Schotte – j.schotte@credendo.com