Cambodia: Succession of external shocks will hit the economic outlook

Event

Over the year, Cambodia has been hit by several external shocks on the political and economic fronts, which could negatively impact its future economic outlook and stability. Firstly, Trump’s import tariff war presented itself as one of the world’s harshest for Cambodia. However, after trade negotiations, the US rate was sharply cut from 49% to 19% – in line with most regional competitors – and zero tariffs could apply to some products. In exchange, Cambodia provided large concessions, amongst which zero tariffs on US goods and mutual recognition of regulatory provisions in various sectors. Secondly, in July, Cambodia entered in a five-day military conflict with Thailand, fuelled by historical territorial disputes. After a ceasefire was reached later in July, both countries signed a US-brokered peace agreement on 26 October during the ASEAN summit in Kuala Lumpur, wherein the withdrawal of heavy weaponry from contested zones and the presence of a temporary observer mission was agreed.

Impact

The peace deal with Thailand was a welcome short-term diplomatic achievement, but very fragile. It has recently been suspended after renewed border clashes. Although both neighbours have interests in stabilising their relations, and are under US pressure to do so (threat of higher tariffs), the absence of a plan aiming at resolving their border dispute in the long-term makes it a persisting bone of contention, with the risk of further escalation in the future.

In addition to heightened security risks, Cambodia is facing rising diplomatic and political risks related to its widening digital scam centres. As in some other south-east Asian countries, those activities appear to have sizably expanded over the past years, making them new international hubs for online scamming and human trafficking, and would represent billions of US dollar of cyber financial fraud. As a result, last October, the US – followed by the UK and South Korea – imposed sanctions against 146 people and entities connected to the Prince Group, a major conglomerate in the country. Consequently, weakened reputation could also affect future foreign investments.

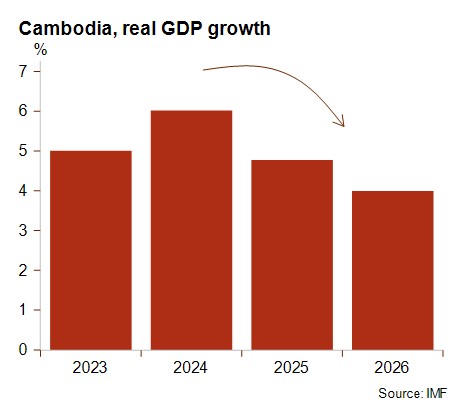

On the economic front, US tariffs and the global economic slowdown are clouding the outlook. Despite an (asymmetric) bilateral trade agreement, the dominance of the US market (nearly 40% of Cambodia’s total export of goods), especially in Cambodia’s garment sector (on which a 19% US rate applies), makes it exposed to higher US tariffs. The uncertainty and volatility of the US trade policy is a risk. Moreover, military tensions with Thailand will impact cross-border trade and workers’ remittances, and could also affect tourism, a major source of foreign currency. All those factors are expected to contribute to the slowing of GDP growth, from 6% in 2024 to 4.8% in 2025, and to 4% the next year. Therefore, macroeconomic fundamentals – which are relatively good with low external and public debts – are likely to weaken. The current account deficit is notably expected to deepen further in 2026. On the other hand, a further deepening trade with the ASEAN could mitigate the net impacts.

Furthermore, Cambodia could be hit by shifting supply chains as the US threatens to penalise countries allowing re-exports from China or from Chinese factories based in Cambodia. The impact could be hard for Cambodia, which benefits from the “China+1” strategy in shifting global supply chains. The latest trade agreement shows that Cambodia is willing to continue to cultivate tight relations with the US, while preserving close financial, economic and political links with China, at least in the medium term. Geoeconomic fragmentation will nevertheless complicate this balanced strategy.

In this difficult and uncertain political and economic context, Cambodia’s risk ratings remain unchanged.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com