Egypt: Middle East conflict weighs on economic recovery

Event

The conflict in the Middle East is impacting countries not directly involved, particularly in Asia and Europe, through disrupted supply chains and higher commodity prices. Egypt, while not located in these regions, is also vulnerable to the fallout from the conflict, given its status as a net energy and food importer, its reliance on the Gulf countries and its still constrained macroeconomic buffers.

Impact

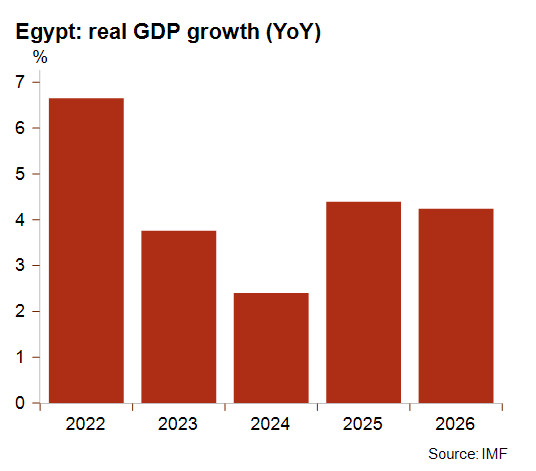

Over the past two years, Egypt’s macroeconomic conditions have been stabilising, and the acute liquidity pressures experienced between 2022 and 2023 has eased as a result of several factors. Firstly due to the authorities’ economic reforms, in particular the shift to a more flexible exchange rate regime, lower commodity price pressures, strong remittances inflows and solid tourism sector performance, but particularly thanks to the substantial external support of regional partners (especially the UAE and Qatar) and multilateral institutions (such as the IMF and the World Bank). In this context, growth began to recover, inflation gradually declined and liquidity conditions improved.

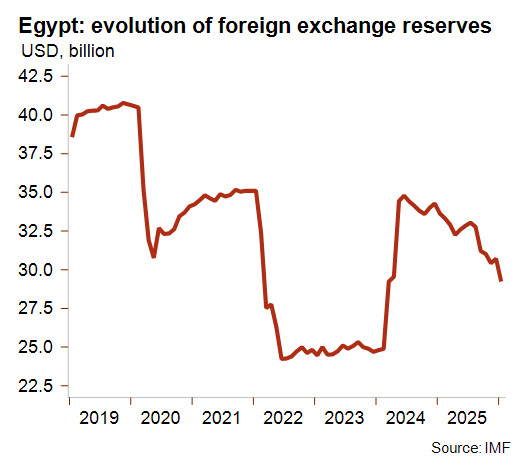

More recently, however, Egypt has faced renewed headwinds, resulting from the conflict in the Middle East, particularly through balance of payments pressures. Since the start of hostilities, Egypt has experienced rapid capital outflows, which have also exerted pressures on the Egyptian pound. Moreover, the import bill is expected to rise amid higher commodity and other imported goods prices, as a result of the blockade of the Strait of Hormuz. At the same time, key sources of foreign exchange earnings could also be adversely impacted, as the GCC countries are important contributors to private transfers and tourism revenue. These important pressures could further intensify if the conflict were to escalate further. In such a scenario, key risks for Egypt would be further increase in energy and food prices, another potential suspension of gas flows from Israel and disruptions of maritime traffic in the Red Sea by the Iran-backed Yemeni militia, the Houthis – which would undermine the timid recovery of traffic through the Suez Canal, another key source of foreign exchange earnings. Depending on the evolution of hostilities, the current account deficit could widen significantly. In this context, economic activity is being adversely affected by rising inflationary pressures and disruptions related to energy-saving measures implemented to limit the risk of energy shortages.

On the positive side, the reforms implemented in recent years have strengthened the country’s buffers. The move to a flexible exchange rate regime and the reduction of subsidies should help improve fiscal balances and foreign exchange reserves. The IMF disbursement of about USD 2.3 billion under the EFF and RSF programmes in late February should also support external buffers. Nevertheless, the macroeconomic situation remains constrained, as indicated by another declining trend in foreign exchange reserves over the past year (see graph) and the very weak public finances. Interest rate payments represented about 75% of fiscal revenues for FY 2025-2026, a very high level, and public debt amounted to about 85% of GDP. Ultimately, this could limit the capacity of the country to absorb shocks.

Considering Egypt’s macroeconomic vulnerabilities and the high degree of uncertainty regarding the evolution of the conflict in the Middle East, Credendo downgraded Egypt’s short-term political risk classification (representing the liquidity of a country) to category 6/7.

Analyst: Andres Hernandez Cardona – a.hernandezcardona@credendo.com