Hungary: Post-Orbán era suggests political reset, market optimism and EU re-engagement

Event

Hungary’s parliamentary elections on 12 April 2026 marked a historic political shift, ending Viktor Orbán’s 16‑year rule. The vote was also notable for recording the highest turnout in a Hungarian general election since the fall of communism in the early 1990s, underscoring the scale of public mobilisation behind the change. The opposition Tisza (Respect and Freedom) party, led by Péter Magyar, secured a landslide victory, winning 138 out of 199 seats in parliament and achieving a two‑thirds constitutional majority. This grants the new government broad powers to revise key laws and institutions that have long been shielded by supermajority requirements.

Impact

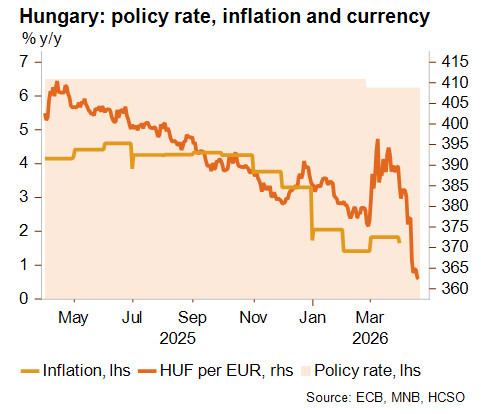

The financial markets reacted swiftly and positively to the election outcome, making Hungary one of the standout performers in global markets immediately after the vote. Moreover, the Hungarian forint strengthened sharply, appreciating by about 3% against the euro (see graph below) and reaching a four‑year high, while the benchmark BUX equity index surged by nearly 4%, significantly outperforming regional peers. Local‑currency government bond yields also declined, reflecting improved investor confidence.

The rally was driven by expectations that the incoming Tisza government will strengthen institutional governance, enhance transparency and normalise relations with the EU (moving from an often obstructive position towards a more cooperative role), addressing factors that weigh on Hungarian assets. Indeed, under the previous administration, real GDP growth volatility, high inflation and elevated borrowing costs persistently contributed to a valuation discount relative to regional peers, such as Poland and the Czech Republic.

Market participants also anticipated potential benefits for foreign-owned financial institutions with significant exposure to Hungary, including major regional lenders, as the new government may reassess sector-specific levies introduced in recent years. Nevertheless, sustaining the rally’s momentum will depend on credible policy implementation and supportive external conditions, including energy price dynamics, given Hungary’s high reliance on imported energy.

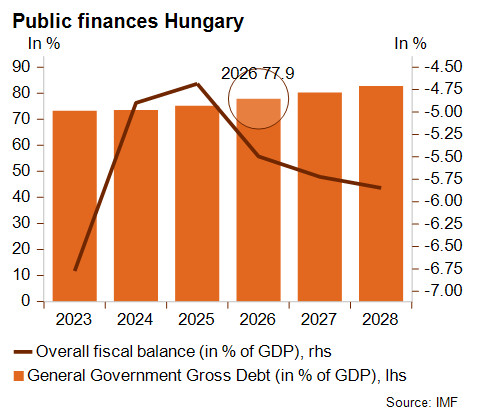

A central priority for the new government will be the rapid unfreezing of EU funds suspended under Viktor Orbán due to rule of law breaches. In total, around EUR 18 billion in grants and loans remain blocked, including nearly EUR 10 billion from the EU’s Recovery and Resilience Facility that will expire at the end of August, as well as cohesion funds that are subject to the EU conditionality mechanism. In addition, Hungary could gain access to EUR 16 billion in defence loans under the EU’s SAFE programme, while compliance with EU requirements could also bring an end to the EUR 1 million a day fine imposed over Hungary’s continued defiance of EU migration law, easing immediate fiscal pressure. However, Brussels is unlikely to release funds upfront: unlike the Polish case, Hungary is expected to demonstrate concrete and irreversible progress before disbursements resume, making credibility and speed of implementation critical despite Magyar’s two‑thirds majority.

Beyond easing near‑term financing pressures, the release of EU funds would enable a broader policy reset, allowing the government to refocus economic strategy on inflation control, wage dynamics and the long‑neglected public services, such as healthcare, education and infrastructure, while improving the investment climate. At the same time, this reform dividend may be partly neutralised by renewed inflationary pressures, as the Middle East conflict is pushing up global energy and commodity prices.

In this context, joining the European Public Prosecutor’s Office (EPPO) is emerging as a key step to rebuild confidence. Magyar has explicitly committed to EPPO accession as part of a broader anti‑corruption agenda, which includes restoring judicial independence, media freedom and academic autonomy. Membership would signal a clear break from past practices, strengthen oversight of EU fund usage, addressing one of Brussels’ long‑standing concerns. While EPPO accession alone will not unlock funds, it would materially strengthen Hungary’s credibility at a time when the European Commission is wary of symbolic reforms. Combined with legislative changes, which could be enabled by the government’s supermajority, EPPO participation could accelerate progress on rule‑of‑law milestones and help reduce governance‑related risk premia.

At the same time, the new government will also intend to anchor reforms around a renewed path towards euro adoption by the early 2030s. Hungary currently falls short of the Maastricht criteria, notably on public debt, fiscal deficit and inflation convergence. Nevertheless, the preparation process itself is economically beneficial, even if euro adoption were ultimately to be delayed or abandoned. Fiscal consolidation, institutional strengthening and macro‑stability measures required for convergence would support growth potential, improve policy credibility and enhance market confidence.

However, the domestic adjustment path will not be frictionless and will take time. The new administration inherits strained public services, a fragile investment climate and entrenched patronage networks, alongside structural energy dependence on Russia. Fiscal consolidation will involve politically difficult choices, particularly given elevated social spending. While access to EU funds would ease near‑term financing pressures and support investment, success will ultimately depend on the government’s ability to convert its strong mandate into durable institutional reform.

At present, Credendo’s business environment risk rating for Hungary is E/G. The outcome of the election and the reform agenda announced by the new government point to a more favourable outlook. Nevertheless, ongoing inflationary pressures associated with the conflict in the Middle East could affect macroeconomic stability in the short term.

Analyst: Laura Pierssens – l.pierssens@credendo.com