South Asia: Covid-19 pandemic is a sharp shock for the sub-region, amplified by India’s economic slump

Economic tumble in South Asia

South Asia, like the rest of the world, has not been spared by the covid-19 public health and economic fallout. In the face of the pandemic and to prevent often poor healthcare systems from being overloaded, countries have implemented multiple containment measures (lockdowns, curfews, quarantines, social distancing, travel restrictions, etc.), which have almost halted or at least severely disrupted economic activity. Applied in the most densely populated countries where the informal economy dominates and where the majority of the population live in rural areas, such measures are difficult to implement in practice and deliver limited effectiveness. That being said, by 11 May, health consequences were still acceptable, with India and Pakistan together reporting fewer than 100,000 infected cases. However, caution is required as new reported cases have been growing rapidly and official data largely underestimate the size of contaminations, notably due to the lack of testing capacities.

This year, many countries could be in recession with the biggest real GDP decline expected in the Maldives (-8% according to the IMF; see graph 1). For some countries, the covid-19 shock came at a bad time. Sri Lanka was slowly recovering from a historic terrorist attack and protracted political instability, whereas Pakistan was in a precarious situation, running austerity policies under an IMF programme to repair deep macroeconomic imbalances. As for the regional engine, India was already in economic crisis after three years of constantly slowing real GDP growth. Therefore, covid-19 will make things worse as India’s growth could be less than 2% this fiscal year (April 2020 to March 2021). The lockdown being extended until 17 May, a recession can no longer be ruled out. Given the profound economic impact and rising social discontent, the Indian government has recently begun relaxing containment measures in the hope of reviving the economy. To mitigate the economic and social impact, South Asian countries have used a mix of expansionist monetary (including heightened credit supply) and fiscal stimuli. It is worth pointing out that the latest GDP growth forecasts are very uncertain as they depend on the duration and severity of the pandemic and potential new waves of contamination – with a special focus on the world’s main regional blocs – and are thus probably too optimistic and likely to be revised downwards in the coming months.

Remittances, tourism and muted export markets are the main transmission channels

The covid-19 shock, in addition to domestic restriction measures, will affect South Asia for some time through various channels. An important one is decreasing workers’ remittances, as they account for a large share of current account revenues for the majority of countries (see graph 2). Most of them will be badly affected by the decline in remittances from the Gulf, where countries are hard hit by the oil crisis, and to a lesser extent Malaysia. The impact will be felt not only on the balance of payments but also on domestic activity through lower private consumption and increased poverty. Their expected recovery in 2021 will greatly depend on recovering demand for oil and how effectively the pandemic is contained.

Tourism is another transmission channel. Given its huge economic reliance on this industry (80% of total foreign exchange earnings) and severe travel restrictions across the world, the Maldives will fall into deep recession this year. Continuing uncertainty around the covid-19 pandemic and the likelihood that tourism will be in cautious mode for some time – as a result of widespread use of social distancing rules and extended travel bans – could prolong the economic slump and increase financial and economic risks significantly beyond 2020. Economies in India, Nepal, Bhutan and Sri Lanka will also be hit by the global tourism shock. In addition, weak external demand and supply chain disruptions will harm exports from India and Sri Lanka. In Bangladesh, the dominant low-cost garment sector (more than 75% of export of goods) is expected to suffer a lot from muted consumption in the EU, its top market, which may recover only slightly in the coming months. That being said, for the whole region, the direct impact of the external demand shock is much weaker than in South East Asia due to low economic openness, India’s large domestic market and historically more protectionist markets. Still, the record capital flight from emerging and developing markets has also hit South Asia. India is the most affected through massive portfolio outflows and reduced FDI inflows. The other countries will be harmed by a freeze or delay in FDI projects related to China’s Belt and Road Initiative (BRI). Although a review of a number of projects and a renegotiation of China’s external loans seem inevitable, most BRI projects will still continue in the medium term.

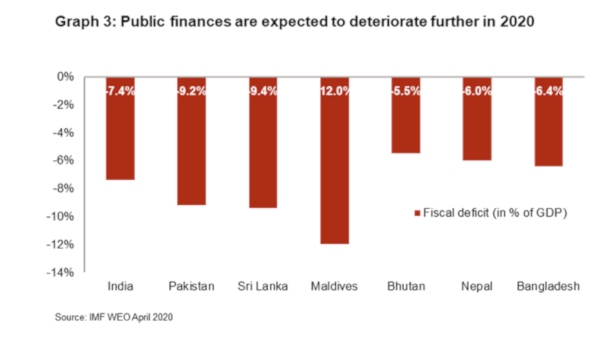

Improving current account balance and a further weakening of poor public finances

The covid-19 shock will affect macroeconomic fundamentals. This year, all countries but one (i.e. Sri Lanka) are expected to see a reduction in chronic structural current account deficits due to the lower contraction of exports of goods and services in relation to imports. This is explained by the largely disrupted economic activity and curtailed oil imports, which are a rare mitigating factor for a region exclusively composed of net oil importers. Public finances, already the poorest in Asia, will worsen through weaker government revenues and higher spending, thereby further widening fiscal deficits (see graph 3). Although fiscal stimuli to support households, businesses and the poor have been limited by the narrow fiscal space, fiscal deficits are expected to climb to a regional average of 8% of GDP whereas public debt will rise to more elevated levels. The lack of fiscal space is a major constraint and could delay recovery. However, India just announced a more vigorous stimulus (equivalent to around 10% of India’s GDP) to boost its anaemic economy as it is also affected by continued insufficient credit supply. In Sri Lanka, the fiscal situation is particularly worrying as government revenues were already low before the covid-19 outbreak.

Multiple external debt moratorium requests until the end of 2020

The health and economic crisis will increase financing pressures and complicate external debt payments. Therefore, with the exception of India, all countries have requested the IMF Rapid Credit Facility and are eligible for the G20 debt service suspension initiative until the end of 2020. Pakistan has already made a formal debt moratorium request while others are expected to follow soon. Some countries such as Sri Lanka and Pakistan, with high external debt payments in the coming years, are seeking extra financial assistance from bilateral and multilateral creditors and also debt renegotiation with China. This should help ease liquidity and debt stresses this year but the situation could remain acute beyond 2020. Meanwhile, since the beginning of the year, depreciating currency pressures, fuelled by record capital outflows in emerging and developing countries, have been moderate until now. Only the flexible Indian rupee (-6%) and the Nepali rupee (-6.5%) have lost more value against the US dollar this year (by 13 May).

Social instability and political risks set to rise

With three of the eight most populated countries in the world being located in South Asia, and a still high share of its population living on limited subsistence resources or in extreme poverty, with no access to public assistance, the covid-19 shock could have dramatic social consequences in the region. Mass job and income losses, higher unemployment, increasing inequalities, a potential food and humanitarian crisis and millions more people plunging into poverty: all those consequences are an explosive social cocktail that governments will face in the future. The risk of acute social tensions, strikes and mass protests is real in Bangladesh, as it is in India, as shown by vivid tensions during the sudden and strict lockdown in a country where the economy is struggling to take off again and unemployment is at a 50-year peak. Moreover, covid-19 has sharply exacerbated religious tensions, which had soared on the back of controversial measures against the large Muslim minority. Social and communal tensions will be hard to manage and could be a hurdle to an economic pick-up. That explains why most governments have launched programmes to support the health sector, the poor and workers (e.g. in the Bangladeshi garment sector), and are actively requesting debt service suspension and international aid. The current crisis could increase the risk of unrest and instability for some years.

This socio-economic crisis could result in political instability that could weaken the popularity of incumbent leaders. This is the case in the Maldives and Pakistan, and potentially also in Bangladesh, where the longstanding ruling party could be confronted with a resurgent opposition and social unrest in the hard-hit crucial garment sector. In India, Prime Minister Modi is firmly in power after a landslide re-election in 2019 but a protracted economic and social crisis combined with religious tensions could make his position more uncomfortable and vulnerable to criticism. In Sri Lanka, even though legislative elections have been postponed, potentially waning support for President Rajapaksa is not likely to prevent his family from holding all the country’s reins.

Credendo ratings: negative outlook and pressures for extra downgrades

The unprecedented health, economic and social shock has a direct impact on country risk assessment and non-payment risks. Bankruptcies and non-payments are likely to soar this year, especially in India, where in addition some sectors such as ports are invoking force majeure events during the lockdown. In terms of ratings, all South Asian countries are now in Credendo’s highest commercial risk category, C (on a scale of A-C), whereas there are downgrades for ST political risk for Sri Lanka (from 4/7 to 5/7) and the Maldives (from 4/7 to 6/7). Thanks to the accumulation of foreign exchange reserves before the covid-19 shock and external foreign financial assistance, other countries have seen their rating unchanged. However, further downgrades are to be expected should the economic crisis be prolonged and the external liquidity situation deteriorate further.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com