Short-term political risk: One country upgraded and five countries downgraded

In the framework of its regular review of short-term (ST) political risk, Credendo has upgraded one country and downgraded five countries.

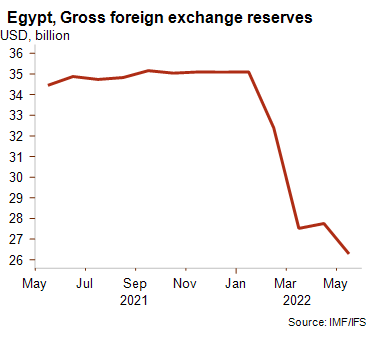

Egypt: downgrade from category 4/7 to 5/7

Egypt’s liquidity has deteriorated since the start of the war in Ukraine and remains under pressure. Undoubtedly, Egypt has been very vulnerable to the fallouts of this conflict. The country – a net oil and food importer and the world’s top wheat importer – has been under the pressure of import bills as a result of the surge in commodity prices triggered by the war. The direct dependence on Ukraine and Russia for wheat imports (85% of total wheat imports) and tourism (around a third of total tourism revenues) has added to the country’s woes. The increase in exports revenues due to higher prices of key exports, such as liquefied gas and fertilisers, and higher Suez canal revenues have not offset the impact on the external balances. Moreover, following the global investors’ flight to safety in light of the war and the ongoing tightening of global financial conditions, Egypt has also experienced capital outflows. These events have led to significant pressure on liquidity and a fall in foreign exchange reserves since the start of the year.

Authorities have taken measures to offset the current pressures, by depreciating the Egyptian pound in March and imposing import restrictions, for example. Additionally, discussions around a new loan programme have begun with the IMF. The country also benefits from the support of GCC countries. Nonetheless, the situation remains challenging given the country’s weak public finances and the challenging global financial and economic conditions.

Ghana: downgrade from category 5/7 to 6/7

The pressure on Ghana’s external balances has further worsened during the third quarter of this year. The levels of foreign exchange reserves fell by a staggering 20% between April and June (down to 2.6 months of import cover), raising liquidity concerns knowing that Ghana lost access to international capital markets and is highly reliant on volatile commodities for its current account receipts. Globally, Ghana has the worst performing currency (after Sri Lanka), as the cedi has depreciated by about 30% against the US dollar since the beginning of the year. Inflation reached almost 32% in July 2022. To deal with inflationary pressure and concerns over foreign exchange reserves, Ghana’s central bank raised its policy rates, at the most aggressive pace in 20 years, up to 22% in August. Moreover, the risk that the central bank will introduce capital controls, which would restrict the availability of foreign exchange in the near term, has increased. On the other hand, Ghana has requested an IMF financial support programme, which would provide additional liquidity if an agreement was to be found with the multilateral lender. Moreover, high gold and oil prices are expected to milder pressure on the external balances by the end of the year. The impact on the real economy is expected to be severe due to soaring financing costs, the rising burden of foreign currency-denominated debt servicing and the soaring cost of living leading to popular unrest.

Pakistan: downgrade from category 4/7 to 5/7

Pakistan’s liquidity situation remains under sharp pressure. Despite the disbursement of a USD 1.2 billion IMF loan (in the framework of the resumption and extension of its IMF programme until June 2023), and the recent one-year rollover of a Saudi loan of USD 3 billion, the country is still facing a very challenging outlook. Devastating floods during this summer have caused severe damages to agriculture crops and infrastructures, which could cost more than USD 10 billion to the country. In addition, Pakistan’s commodity imports could remain high in the coming months, and thus continue to weigh on the cost of living and foreign exchange reserves. In this touchy socioeconomic and financial context, political instability could grow further and threaten the implementation of government policies required by the IMF programme.