Latin America navigates Middle East turbulence well

Event

As the conflict in the Middle East enters its third month, its negative impact on the global economy is becoming increasingly visible. However, Latin America appears relatively insulated.

Impact

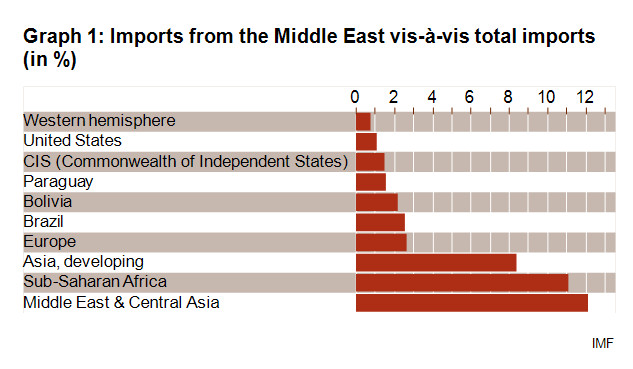

Latin America has limited direct exposure to goods flows transiting from the Middle East, as shown in graph 1. On average, the Middle East accounts for less than 1% of the region’s total imports, well below other regions globally. Even the largest importers – Brazil, Bolivia and Paraguay – source only about 3% of their total imports from the Middle East. Although higher fuel prices are transmitted to the region, Latin America’s many net fuel exports have partially absorbed global fuel demand and benefited from higher fuel prices. This is particularly the case for Brazil and Guyana with record oil exports, and for Argentina with record gas exports. Even Panama, despite being a net oil importer, has cushioned part of the impact of high oil prices through increased canal traffic due to rerouted maritime flows. In addition, unlike parts of Africa or South Asia, the region is not a major recipient of remittances from Gulf Cooperation Council (GCC) countries, despite the Gulf’s role as the world’s second-largest remittance outflow hub. Similarly, FDI inflows from GCC countries into Latin America are limited, reducing the transmission channel through capital flows.

That said, the duration of the conflict and of the disruption of GCC exports matters: if it persists, Latin America will also feel the impact more significantly. The first and most immediate transmission channel is persistently high oil prices, which will particularly hurt net oil-importing countries, especially in the Caribbean and Central America. Higher fertiliser prices represent a second major transmission channel due to the GCC’s dominant role in global supply, providing roughly a fifth to a third depending on the fertiliser. At the same time, Latin America depends heavily on agriculture for current account revenues and liquidity. Indirect spillovers are also emerging. China, South America’s largest trading partner, has imposed export restrictions in response to the Middle East conflict. A prolonged export ban on sulphur could weigh on copper producers such as Peru and Chile, although they currently still have sulphur buffers. Meanwhile, export restrictions on fertiliser could hit Brazil particularly hard unless exemptions are granted.

A prolonged conflict or extended period of reduced GCC exports would also reignite inflationary pressures. Prior to the conflict in the Middle East, most central banks in the region were easing their monetary policy following the 2022–24 tightening cycle. They have since adopted a more cautious stance. If inflation reaccelerates, further monetary tightening is likely and potentially more aggressive than in advanced economies, given that the region is far more exposed to capital outflows. Rising interest rates, while still historically elevated, would add pressure on already indebted sovereigns and corporates as well as on economic growth, which would increase the risk of bankruptcies.

Typically, rising prices, especially for food and fuel, trigger social unrest. In Latin America, high wealth inequality, combined with elevated public debt and limited fiscal room for fiscal expansion, creates fertile ground for social unrest. Road blockades are among the most common and disruptive forms of protest in the region, as currently seen in Bolivia. They can persist for months, severely affecting supply chains, creating goods shortages and even toppling governments, given the region’s heavy reliance on road infrastructure.

Even so, Latin America is relatively resilient compared with most other regions, even under a scenario in which the interruption of GCC goods persists for months. Within the region, the Caribbean stands out as the most vulnerable, given its high dependence on imported food and fuel, which together account for around 40% of imports. As tourism is by far the main source of current account income and accounts for around 60% of total current account revenues, further risk stems from jet fuel price increases and potential shortages. These could weigh on tourism revenues, although the region remains relatively less exposed given the major jet fuel refining capacity in the United States.

Analyst: Jolyn Debuysscher – J.Debuysscher@credendo.com