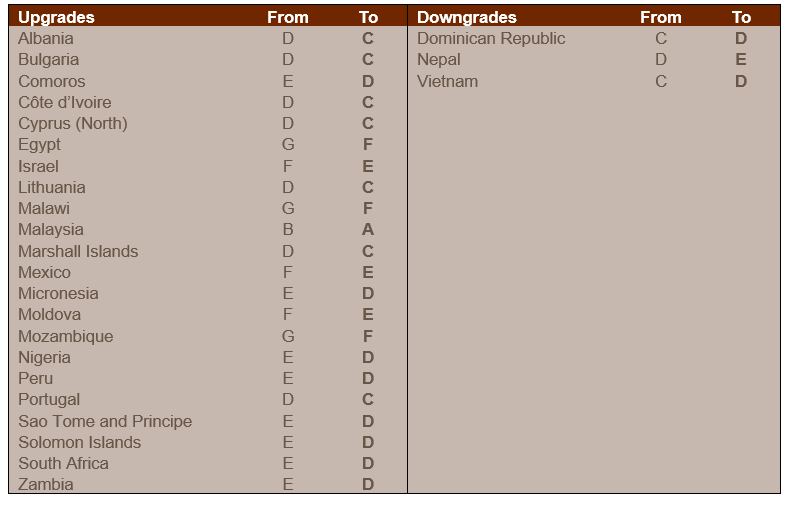

Business environment risk: Twenty-two upgrades and three downgrades

In the framework of its regular review of the business environment risk, Credendo has upgraded twenty-two countries and downgraded three countries.

Business environment risk

- Côte d’Ivoire: upgrade from D/G to C/G

Côte d’Ivoire’s business environment risk classification was upgraded to C/G thanks to strong growth performance and a stable monetary and financial environment. GDP growth reached 6.4% in 2025 and is expected to reach the same impressive level in 2026 as it is driven by the hydrocarbons and mining sectors and strong economic management. The current account deficit should continue to narrow from -2.3% of GDP in 2025 to -1.8% in 2026. In October 2025, President Ouattara secured a controversial fourth term after excluding key opposition figures, which led to widespread protests. Although grievances over the growing democratic deficit remain, protests have subdued and the risk of political destabilisation has moderated again. The government is expected to commit to IMF-backed reforms and fiscal consolidation, which should lead to policy stability and sustained external (donor) support. The deterioration of the security environment in Mali and Burkina Faso poses a rising threat, especially to Côte d’Ivoire’s northern border region.

- Malaysia: upgrade from to B/G to A/G

The year 2025, marked by the US trade war and related uncertainty, is ending on a more positive note for Malaysia. Indeed, on 26 October, Malaysia and the US reached a trade agreement within a comprehensive strategic partnership at the ASEAN summit, including a 19% US tariff on Malaysian goods and zero US tariffs on several exports such as palm oil and pharmaceuticals. In exchange, Malaysia offered preferential market access for US goods (recognising US standards) and a favourable supply of critical minerals, and committed to large purchases of US goods. Though a volatile implementation of the agreement would maintain the risk of US pressures, this agreement should prevent tensions with the US at least in the short term. It is a welcome development in the face of external headwinds, from high US tariffs to weakening global demand, and of increasing domestic competition from Chinese products. Exports might show resilience in the coming months thanks to the contribution of the electronics sector, particularly the booming semiconductors, and more generally to the further deepening regional trade integration. Besides, GDP growth should remain supported by private consumption, that benefits from low inflation (1.3% in October on the back of lower commodity prices) and by eased monetary policy (the central bank cut its interest rate to 2.75% last July). Thus, GDP is still expected to grow by a robust 4% (from an expected 4.5% this year) in 2026. The persisting current account surplus and the Malaysian ringgit’s appreciation, not only against a weakened US dollar but also against currencies from Asian competitors, are additional factors of confidence vis-à-vis the Malaysian economy for remaining on a strong foot in 2026. Hence, Malaysia was upgraded to the best business environment risk category A/G.

- South Africa: upgrade from E/G to D/G

South Africa’s business environment risk classification is gradually improving. A more reliable electricity supply in 2025 has raised private sector confidence and ended a painful energy crisis. Although economic growth remains slow, it reached more than 1% again in 2025 (1.2% in 2026). Inflation will fall below 4% again thanks to the South African Reserves Bank’s (SARB) solid monetary policy. Moderating inflation levels allowed for several downward revisions of the SARB policy rate to 6.75% in December 2025, coming from 8.25% in December 2023. The current account has been balancing around an equilibrium since 2022 and should continue to do so over the coming two years. The value of the South African rand has strengthened against the US dollar over the course of 2025. The 30% US tariff on South Africa has been in place since August 2025, affecting all value-added sectors. The South African government continues to work on mitigation strategies despite the US administration’s outrageous attacks on its domestic politics. On the upside, progress in strategic policy reforms with regard to critical minerals, renewable energy and infrastructure, will support substantial investment inflows and economic growth over time.

- Zambia: upgrade from E/G to D/G

After a profound financial crisis and a severe drought, economic prospects turned favourable again in 2025, leading to a gradual upgrade of the business environment risk classification. Economic growth reached 5.8% in 2025 and should grow to 6.4% in 2026, driven by mining activity (especially copper), infrastructure investments, electricity generation recovery and private sector participation. Inflation was high for years due to food price pressures, supply shortfalls and a depreciation of the kwacha. By end 2025, inflation is expected to fall to 11%, coming from 17% last year. Should the Bank of Zambia maintain its tight monetary policy going forward (policy rate at 14.3%), inflation could be tempered to 8% or 7% as of next year. The current account projections are positive with a surplus as of this year, while policy performance is strong and the agreement on debt restructuring will support investor confidence. However, exposure to adverse climate shocks and a slow recovery of rainfall levels are important risks, as are the volatile global copper prices and possible challenges to fiscal reform implementation in the run-up to the 2026 general election.