Short-term political risk: Nine countries (incl. Angola, Ecuador and Oman) upgraded and four countries (incl. Myanmar) downgraded

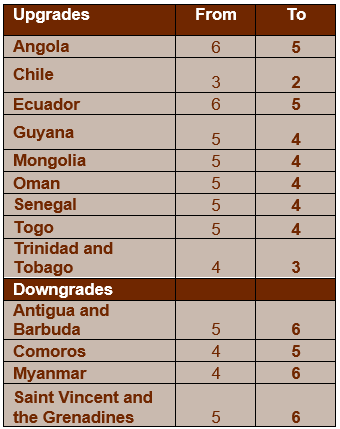

In the framework of its regular review of short-term (ST) political risk classifications, Credendo has upgraded 9 countries (Angola, Chile, Ecuador, Guyana, Mongolia, Oman, Senegal, Togo, and Trinidad and Tobago) and downgraded 4 countries (Antigua and Barbuda, Comoros, Myanmar, and Saint Vincent and the Grenadines).

Angola: upgrade from 6/7 to 5/7

Covid-19 caused a sharp drop in both Angola’s imports and exports, resulting in a small current account deficit in 2020. As of this year, the current account is expected to turn into a small surplus again thanks to more favourable international oil prices. As the outflow of capital is set to slow down, the external balance of payments should remain positive, allowing for foreign exchange reserves to further accumulate after they reached about 7 months of import cover by the end of 2020. Although in nominal terms, gross foreign exchange reserve levels were cut in half since 2013, the liquidity position in relative terms is improving. However, the availability of hard currency in the market remains restricted and capital controls still exist. Nevertheless, over the past 2 years the BNA (Central Bank of Angola) has been focussing on enhancing exchange rate flexibility and gradual elimination of foreign exchange restrictions to increase competitiveness, enhance the potential of absorbing shocks and strengthen general liquidity. Following the confirmed improvement of Angola’s main liquidity indicators since the end of 2020, Credendo decided to upgrade the country’s short-term political risk classification from category 6/7 to 5/7.

Ecuador: upgrade from 6/7 to 5/7

Liquidity indicators have vastly improved in the fully dollarised economy. First of all, the USD 6.5 billion IMF loan (approved in August 2020) in combination with higher oil prices (Ecuador is an oil exporter) led the low foreign exchange reserves to rise to their highest level in 20 years (covering almost 3 months of imports at the end of December 2020). Secondly, the current account also improved and is expected to post a small surplus this year of about 0.5% of GDP. Furthermore, short-term external debt decreased and stands at a moderate level. Lastly, in April Lasso was elected president. He will take office on 24 May and is expected to continue incumbent president Moreno’s orthodox macroeconomic policies. Essentially, the IMF agreement that forms the basis for policymaking is expected to continue to be the linchpin of policymaking, likely boding well for the liquidity indicators. For these reasons, Credendo decided to upgrade the country’s short-term political risk classification from category 6/7 to 5/7.

Oman: upgrade from 5/7 to 4/7

When the oil price collapsed at the beginning of 2020 due to the onset of the Covid-19 crisis, Oman’s liquidity position was put under pressure since its oil revenues account for around 65% of total foreign exchange receipts each year. Additional pressure was caused by the significant amount of external debt that the country needed to service in a context of more adverse global financial conditions. This led to a downgrade of the short-term political risk classification in April 2020, from category 3/7 to category 5/7. One year later, we’re seeing a steady recovery of the oil price and more supportive global financial conditions. This combination is expected to reduce the current account deficit from 10% of GDP in 2020 to 6.4% of GDP in 2021. At the same time, global financial conditions have eased and global capital flows towards emerging markets picked up again. Given Oman’s significant external debt service needs, this is very positive news for the country. Lastly, Oman has been running significant twin deficits since the oil price collapse of 2014. In recent months, the sense of urgency to reduce macroeconomic imbalances seems to have increased as for example a number of initiaves have been taken to reduce the public deficit (which amounted to 17.3% of GDP in 2020). Therefore, it was decided to upgrade the short-term political risk classification to category 4/7. Nevertheless, risks remain firmly on the downside given the uncertain impact of a possible rise of global interest rates on global financial conditions, and uncertainty about Oman’s effective ability to implement the difficult measures needed to reduce the public deficit and thereby help preserve macroeconomic stability.

Myanmar: downgrade from 4/7 to 6/7

Since the military coup d’état of 1 February 2021, the economy has collapsed. Indeed, anti-coup protests and wide civil disobedience have largely disrupted business, port and banking activities, led to the closure of several factories (notably in the important garment sector) and the decision of several foreign investors to leave the country or suspend their activities. This economic near-paralysis is occurring in an already weak economic context due to the persisting impact of Covid-19. Moreover, the latest sharp Covid-19 waves in South and South-East Asia could further hit the country by favouring the virus spread and hindering testing and vaccination plans. In the short term, the political crisis is expected to continue between an increasingly repressive army and an informal-unity national government supported by armed ethnic groups. Hence, the economic outlook is gloomy and very uncertain. In the current chaotic context, no recent data has been made available over the past months. However, foreign exchange reserves, which covered nearly 5 months of imports at the end of 2020, are expected to decline significantly this year as a result of weak exports, tourism receipts and FDI inflows. Also, in practice, recent reports highlight the restricted access to foreign exchange which is increasingly hindering international payments and raising transfer risks. Given those tough circumstances, Myanmar has been downgraded from category 4/7 to 6/7.