Bangladesh: Higher socio-political tensions can be expected amid rising commodity prices and a deteriorating external environment

Event

The war in Ukraine and disruptions in imports from Russia are hitting Bangladesh’s continued economic recovery. The pronounced commodity price shock, and more particularly higher fuel and food prices, could have destabilising social and political effects, as recently highlighted by nationwide anti-government protests. Not only domestic demand will suffer from gloomier economic conditions but weaker western demand will also harm the dominant garment exports. Hence, economic growth is expected to reach lower levels this year.

Impact

The Covid-19 pandemic has affected the Bangladeshi economy, but its overall impact on macroeconomic fundamentals has been relatively subdued. The country’s usual economic resilience, supported by remittances buffer (at record levels in FY 2021 that ended in June 2021) and the robust garment sector, allowed the country to be an exception in maintaining positive growth in FY 2020 (+3.5%) before rebounding by 5% in FY 2021. Now, new shocks are hitting the economy. The war in Ukraine is driving high inflation pressures (food and energy), leading to disruptions in food imports from Russia and Ukraine and adding pressures on the budget with extra spending (food subsidies were announced last month) to ease the socio-economic burden and prevent food insecurity risks. All those factors will translate into weaker growth forecasts. Consequently, the latest IMF’s GDP growth forecasts for Bangladesh (+6.6% in FY 2022 and +7.1% in FY 2023), published in March, and based on data until mid-February, will certainly be revised down later this month.

In this difficult socio-economic context, fast rising living costs triggered large protests and strikes in the end of March. If energy and food prices stay high for a long period, this will not only fuel risks of social instability but also of political magnitude. Social tensions could progressively affect the strong control of long-serving country leader, PM Sheik Hasina, on the political landscape and possibly contribute to revive the weakened and fragmented opposition.

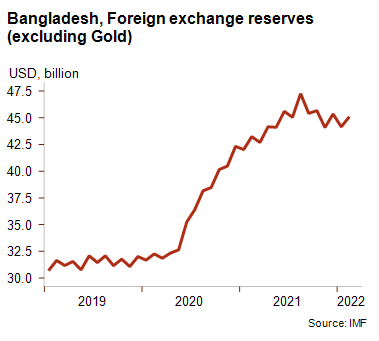

For the moment, the country’s external liquidity remains good. Indeed, in the first year of the pandemic, foreign exchange reserves increased thanks to a stronger contraction in imports compared to exports and robust workers’ remittances, and have remained stable since then.

Hence, currently, their import cover is rather comfortable at 6.5 months, but likely to decrease in the one-year outlook. However, Bangladesh’s short-term political risk rating, quite stable in 3/7 in the near term, might be under pressure at some point in the future. The short-term external debt-to-current account receipts ratio is moderate and Bangladesh’s liquidity is expected to be hit by the negative fallout of the war in Ukraine. This could result in a widening of the current account deficit – i.e. falling global demand for garments, rising imported fuel and food prices and declining remittances (as the very high levels reached in FY 2021 were partly explained by temporary government incentives to remit money from overseas) – and a slowing down in foreign exchange reserves accumulation.

Regarding the business environment risk, the Bangladeshi taka remained largely stable (-1.6%) against the US dollar between March 2021 and March 2022, partly thanks to some interventions of the central bank. However, rising inflation (at 6% y-o-y in March) and a deepening current account deficit will put more pressure on the taka in 2022. Taking into account the weaker GDP growth ahead, the rating outlook (D/G) is negative as well. Moreover, the risk of further Covid-19 waves has not disappeared. Bangladesh was hit by several waves, the sharpest being recorded last summer (Delta variant) and in January-February 2022 (Omicron variant) due to slow vaccination rate. Nevertheless, two-thirds of the population is now vaccinated and the pandemic is expected to be a more minor downside risk in the months to come.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com