Bangladesh: External liquidity support is coming up amid heavy energy imports

Event

In the end of July, Bangladesh approached the IMF for financial support. The country is seeking extra liquidity support from multilateral lenders (World Bank and Asian Development Bank) and bilateral creditors. Those loans aim to strengthen the country’s eroding liquidity amid high commodity prices.

Impact

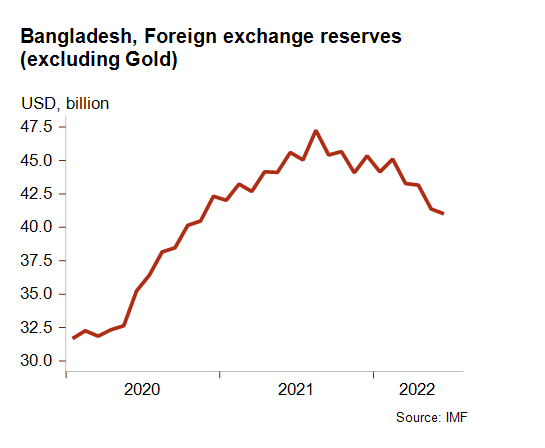

Details of the requested IMF loan – possibly up to USD 4.5 bn, partly coming from the IMF’s Resilience and Sustainability Trust (RST), which aims to help combat climate change – are yet to be negotiated. Bangladesh’s request is another example of liquidity pressures that South Asian countries are currently facing, particularly due to the fallout of the war in Ukraine, which further increased commodity prices. Like in Sri Lanka and Pakistan, high food and fuel prices have detrimental consequences on macroeconomic fundamentals and lead to energy shortages and frequent power cuts. The current account deficit has been widening fast, to more than 3% of GDP (in FY 2021-22 that ended in June), as a result of costly imports and decreasing remittances. The taka has lost 10% against the US dollar since May (after several small devaluations in May and June) whereas inflation has been fluctuating around 7.5% since May. Nevertheless, Bangladesh is in a relatively much better position thanks to stronger liquidity buffers, a resilient economy, low external debt and political stability – though unrest risks are on the rise (see below). Indeed, in spite of their downward trend (since their historic peak in August 2021)further exacerbated by the conflict in Ukraine, foreign exchange reserves were still adequate to cover five and a half months of imports in June and six times the external debt service. The country’s short-term debt is also stable at less than 25% of current account receipts. Therefore, Dhaka’s quest for external financial support looks more like a precautionary move, given the challenging outlook in the one-year period, notably regarding high energy prices and risks of global recession.

Bangladesh’s solvency is better as well. External debt is low and public debt is mainly domestic with an external share remaining below 20% of GDP, and thus less exposed to the global monetary tightening. However, in order to reduce the chronic fiscal deficit, the government recently decided to sharply cut fuel subsidies, thereby leading to a 40% fuel price hike. The resulting large protests and potential boost to inflation illustrate the socio-economic risk for the government if it takes unpopular fiscal measures, including raising Asia’s second-lowest government revenues (after Sri Lanka) – less than 11% of GDP in the end of June 2022 – to facilitate access to a larger IMF support. Heightened political instability might be at risk in the short term as high cost of living is fuelling discontent. That’s why, for political reasons, it is uncertain whether long-serving PM Sheikh Hasina’s government will discuss a conditional IMF programme that goes beyond the RST.

In this difficult economic context, the ST political risk rating (in category 3/7) will be under downgrade pressure in the next months, whereas the business environment risk could still show robustness. Stronger spending in development projects could indeed mitigate the probable economic slowdown – from an expected 6.4% in FY 2021-22 – driven by the weakening global demand and garment industry and by lower private consumption. As for the MLT political risk rating, at this stage, it is expected to stay in a stable 4/7 category this year.

Analyst: Raphaël Cecchi – r.cecchi@credendo.com